The HindeSight Letter

ISSUE 129 - Nov/Dec 2025 (Published January)

OVERVIEW

Long-term readers will be used to my year-end letter that merges November and December into one as time runs out like the proverbial late dentist appointment. Apologies all the same. The holiday season and arrival of the New Year always gives us opportunity to sit back and assess the world, both as a place to live and enjoy and with relation to investments, of course.

I was struck by an article written by legendary war correspondent, John Simpson who pronounced that he had never seen a year so worrying as 2025. The last paragraph of the article read;

LINK: Here

I doubt anyone predicted that the Ukraine-Russian war would be entering its 5th year, in February 2026, but arguably its 12th year, if the 2014 Crimea invasion is used. Bearing in mind our recent history of two world wars saw four and six years duration, you could believe we must be running out of support, either domestically or abroad, regardless of Trump’s best efforts. However, when I google a list of wars by timeline, I find anything from 774 years for The Reconquista, which saw the Christian armies rid Al-Andalus (Modern-day Spain) of the Muslim kingdoms to the shortest recorded conflict of Anglo-Zanzibar war of just 38 minutes! So way open.

Wikipedia: List of Conflicts By Duration

John Simpson is infinitely more qualified than me to write of worrying war histories in 2025 and clearly the outlook for 2026 and beyond would appear less than optimal. Whether it is the widely expected Chinese invasion of Taiwan, that is already hotting up amid Sino-Japan spats of late or US global police power against Iran, Venezuela et al, while nothing resolved in Ukraine, we should be as worried as John Simpson suggests, I fear.

Somewhat regretting it now, but I finally got around to watching Oppenheimer over the festive period. An incredibly powerful movie with Cillian Murphy playing the lead role tells the story not just of the development of the atomic bomb but the discussions of expected nuclear war deterrent, which did happen for 80 years since the only conflict use by the US against Japan in 1945. Clearly, a worry now is that with far too many regional conflicts growing and several countries in possession of nuclear weapons, we have to keep Oppenheimer’s faith that the threat of self-annihilation is too apparent to all.

Unfortunately, the world has seemingly entered a new cycle of instability globally and alliances and treaties that have moderated conflicts for decades are now being challenged. It doesn’t help by any means, especially in Europe that many of the current politicians are far below historic par in terms of competence, domestically or on the international stage. It is no surprise at all that according to recent reports, the US administration aims to persuade Austria, Hungary, Italy and Poland to distance themselves from the EU and the UK and align more closely with the United States. It’s not rocket science to observe these nations are making better decisions on immigration and defence than the rest of Europe.

As for the UK, the “one-term” Labour government will be hard stretched to become more unpopular and deemed more incompetent in 2026 than 2025 but no doubt, they will try. We had some soberingly news locally late last year with some farmers committing suicide that intended to avoid the April 1st inheritance deadline for a 20% tax on family farms/businesses over £1mil, a tragedy which has been seen across much of the UK. It will be of no consolation to their surviving families that yet again Labour has had to reverse a poorly-thought out plan and now the inheritance threshold has been raised to £2.5mil.

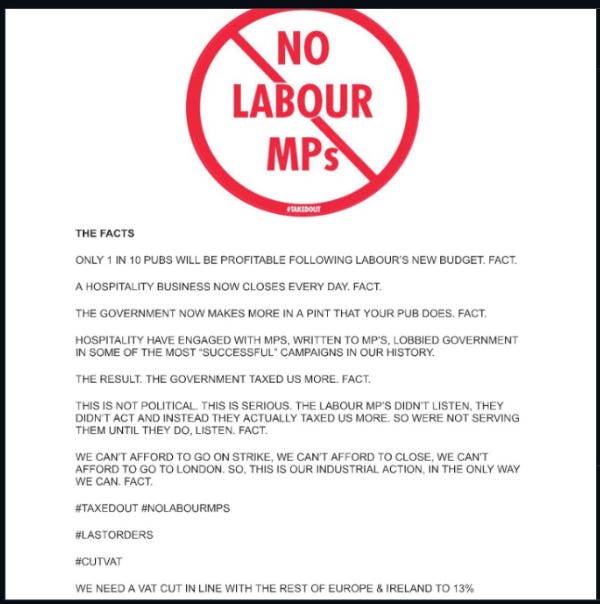

It doesn’t matter where you look, the working population in the private sector is in open revolt against the government, the latest visual is the growing number of pubs, bars and restaurants that are displaying signs barring Labour MP’s from their premises due to the horrendous tax increases that the hospitality industry faces. Of course, with pubs closing at a rate of one per day across the UK, it won’t just be the Labour politicians who will be resigned to drinking at home soon.

Meanwhile, the burgeoning state’s public sector workers enjoy 8% annual pay increases, 20 sick days a year and golden-plated pensions but with the private sector’s declining profits and rising unemployment having to fund this fiasco, it’s only a matter of time before a recession/ collapse and the piper will have to be paid.

I did like this comment by Gary at Gibraltar Corporate Partners, “Watching Rachel Reeves point at the FTSE 100 and declare the UK economy “thriving” is like a landlord bragging about property values while the roof caves in and the boiler’s packed up”. Of course, the stellar +22% performance by the FTSE 100 this year is more driven by international profits with the cheap £GBP currency enhancing that, but I very much doubt that Rachel has been briefed on that fact. The FTSE 250, much more representative of UK Ltd is up just 9% , one of the world’s worst performers which tells a more relevant story.

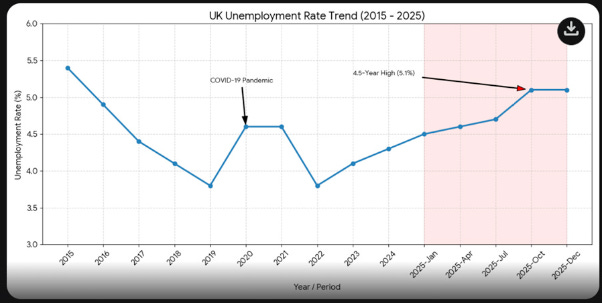

Everywhere I go, I hear the same-Headcount is sensitive. Ie. Very, very difficult to justify! Whether it is the rising costs of National Insurance and minimum wage levels, especially for the younger workers or real concerns about the Employer Rights Act that became law in December- companies, large and especially small are not hiring and actively shedding staff to cope. Official figures show the number of payrolled employees has fallen by 187,000 in the 12 months to October 2025 and continuing to fall as the unemployment rate rises above 5%. The remaining options of finding a job in the public sector or going on the dole, both at least benefit from minimal workloads and loads of sick days is not the best plan for UK growth potential.

Much of the discussion around the country is typically English sounding very much like WW1 trench humour-no pubs, no farms, no justice and cancelling local elections (afraid of losing) like a communist state. We often hear Sir Keir Starmer and his cohorts use the phrase “Sensible reform” but as one journalist wrote, “ You can say it as many times as you like, but if most of the country think it’s bullshit, it probably is!”. The Peter principle is so apparent within the government ranks that it’s hard to know where to start although I did like billionaire Nick Candy’s comment regarding David Lammy, Justice Secretary, “He wouldn’t get a job as a janitor in any of my companies”.

My personal favourite in recent months that had me ROTFLMFAO at the insanity was Rachel Reeves being asked on BBC News about how people were expected to pay for her new mileage-based tax for electric vehicles. Her answer was, “When they have their MOT, the mileage is taken” But, when the presenter told her that new vehicles, (which most of the electric vehicles would be) didn’t need an MOT for the first three years, she was completed stumped! Hmmm.

To me, that just sums up every policy that has been brought in to date, no real planning, no practical framework and no understanding how real people live and the new choices they will make if you deliver ridiculous policies. Whether it’s getting rid of 800-years history of trial by jury or adding VAT on private schools, the country is going down the tubes faster than a lead ballon in a vacuum!

The old adage from the classic film, Alice in Wonderland seems very apt for the Labour party currently, “If you don’t know where you are going, any path will get you there”!

I must move on soon on this topic as I fear I am danger of repeating myself and no writer wants that on their epitaph. Older readers will well remember The Sun’s headline the day before the 1992 UK General Election regarding leaving the country if Labour leader Neil Kinnock won the election. At the time, I was on the streets of Basildon helping to campaign for the long-term conservative MP, David Amess who was victorious in holding his seat then. Tragically, he was murdered in his constituency surgery by a Somali immigrant in a terrorist attack in 2021 after almost 40 years of service as an MP. Labour lost the election, people didn’t leave and the lights stayed on and the country prospered for decades afterwards.

At a neighbour’s 80th birthday party last year, I heard his story of leaving the country in 1976 as a young man because of the state of the nation under Harold Wilson’s/ Callaghan’s disastrous terms and we talked of the same drain going on now. While a poorly researched article, IMO by The Economist (When did they join the BBC and become so left-wing biased?) on net migration numbers suggested otherwise, it is clear to anyone that there is some real movement going on here. But, it needs to be grouped correctly. Sure, super wealthy entrepreneurs and non-doms have been first out the door, well-off wealthy UK citizens worried about inheritance tax at 40% instead of 4% overseas are keen to re-domicile abroad before an exit tax and the incoming less wealthy returners seem to be in the upper age bracket, arguably coming back for NHS healthcare. But, the group that should worry the most is the 25-40 year-olds who are looking to build wealth and realise they can’t do it here that easily at this current time.

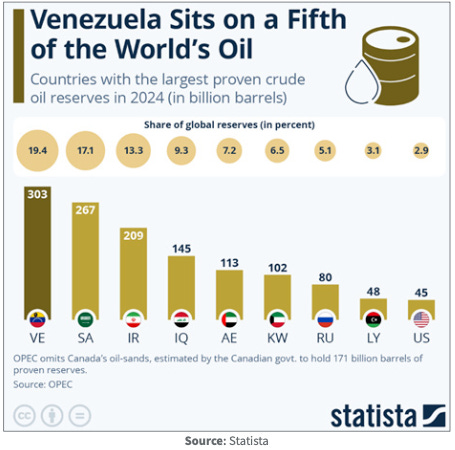

The Venezuela episode at the opening of 2026 seems to have set the stage for some continued volatility this year although I worry that some asset classes like equities are not going to enjoy the best of returns that people cheered in 2025.

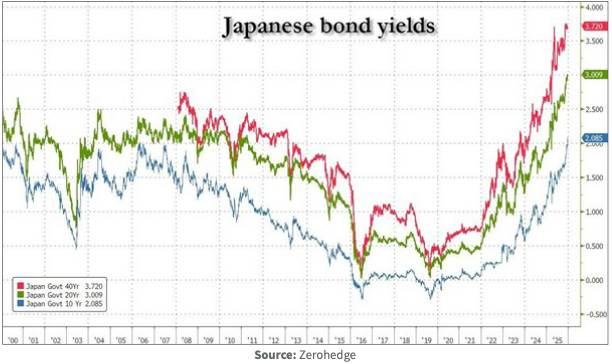

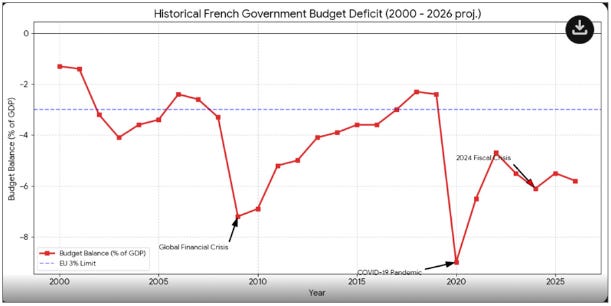

I will sign off the Overview section with four charts below that are top of my concerns for major asset classes;

Japanese bond yields

French budget deficits

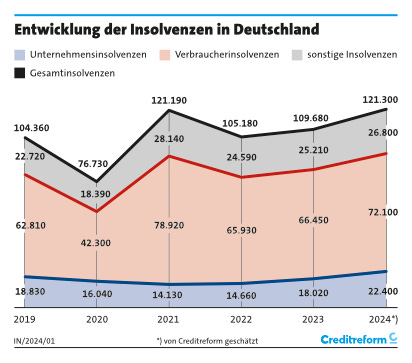

German insolvencies

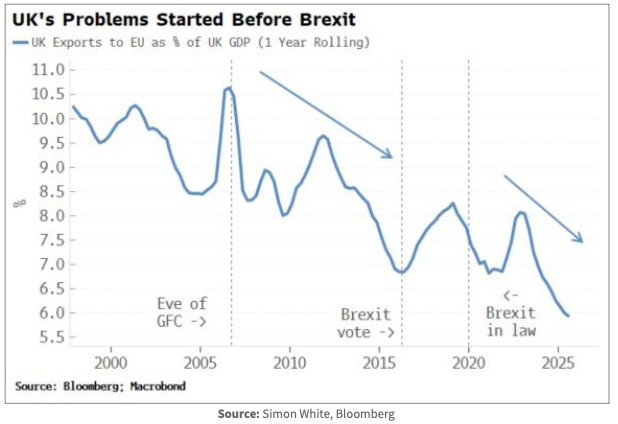

UK’s export issues

Of course, it does seem even more farcical that Sir Keir Starmer is trying to engineer a reverse Brexit policy just at a time when Europe and the single currency looks more prone to failure than at any time in its 25-year history. Throw in the US keen to reduce NATO commitments and Russia resurgence and easy to argue that the worse place to be for all reasons is Europe.

INVESTMENT INSIGHTS

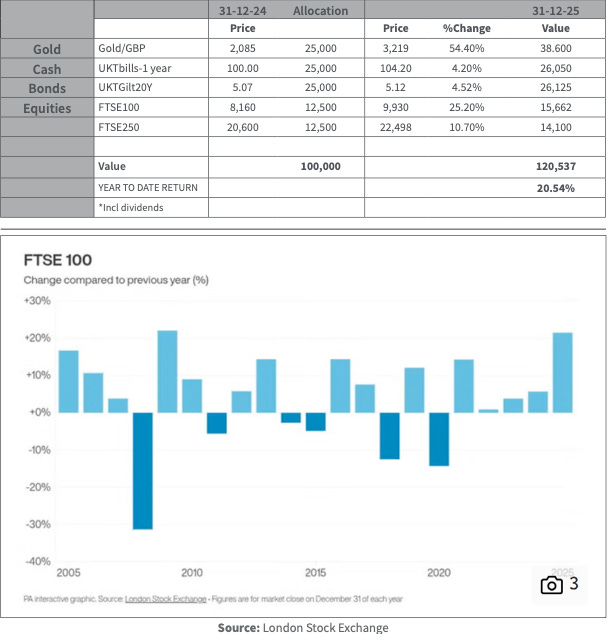

It’s that time of year where it’s good to take stock and look at what worked in the investment world and what didn’t. In general, 2025 was a storming year for anyone who had precious metals as a good part of their portfolio. Whether it was the physical metal itself or the relate mining equities, it was truly a sweet spot for returns. The Permanent Portfolio, (PP) that we publish every month here to keep investors focussed on having reasonably gold exposure has had its best year in a long while, +20.54% with gold up 65% being the main driver. The FTSE 100 had its best year since the post GFE 2009 stormer at +25% including dividends which is not to be sneezed at, despite the FTSE 250 lagging quite a bit, unsurprising given the state of the economic numbers in the UK. The FTSE 100 big winners were a split of miners, banks/insurers and defence stocks for the most part but even UK/US government bonds had reasonable returns as yields fell while paying out the coupon interest. Defence spending and geo-political worries driving precious metals while banks are benefitting from the steepening yield curves. (Borrow short-Lend Long =Profits etc).

Bitcoin, oil and Japanese government bonds were the most obvious losers on the main screens and the chart below showing the long-term ratio of silver to oil tells a good story.

We will notionally be re-balancing the Permanent Portfolio for the new year back to the 25% weightings across the board which is a simple straight forward rule but many investors will be wondering what 2026 will bring in the major asset classes.

As we have mentioned in the Overview section, we have heightened concerns regarding downside volatility given the valuations of the equity markets and the free- money spigot of zero Japanese rates being turned off after decades of support. We would be very wary of long-dated government paper, such that any recession concerns that sees lower central bank interest rates, we would favour the front end of fixed income markets. The UK and the European economies are far, far from strong. Regulation, taxation, high energy costs and public sector/ state enlargement with increasing indebtedness haven’t held the equity markets back this year but I fear that it’s only a matter of time.

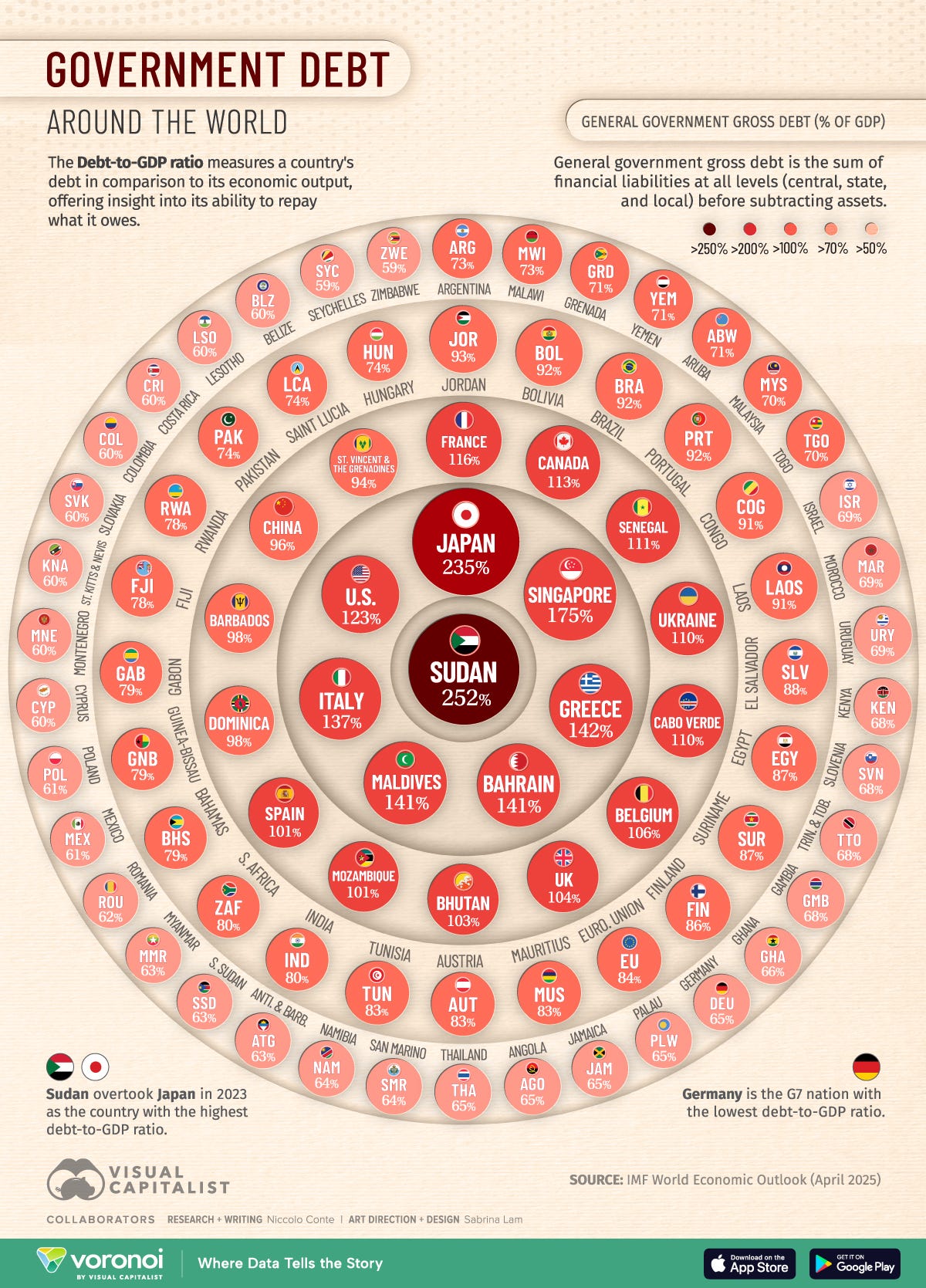

The global debt visual below coupled with the constant money supply increases tell us that currency debasement and inflation are either desired outcomes or natural results so that continues to tell us that gold and its derivatives are likely to be ongoing beneficiaries, even without the geo-political backdrop. All real assets are certainly a safer bet than paper assets at this juncture.

The Permanent Portfolio

AS USUAL, A SMALL SELECTION OF CHARTS THAT I THINK ARE RELEVANT.

HINDESIGHT PORTFOLIO UPDATE (DECEMBER 2025)

There were two CLOSE alerts for the HindeSight Portfolio in December 2025;

CLOSE ALERT- Phoenix, (PHNX) Absolute Return +50.66% (incl dividends), Relative Return, +40.35% (FTSE100), Holding Period, 292 days

CLOSE ALERT-Rio Tinto, (RIO), Absolute Return +34.88%, (incl dividends), Relative Return, +6.61%, Holding Period, 667 days

With two more profitable closes and no add alerts, the HindeSight portfolio for single stocks has shrunk considerably this year. Much of this reflects our belief that UK equities have had an amazing run in 2025 in general but even more so our selections. But, also it should be understood that the parameters that the HS model uses are currently not generating single stock equity selections where the expected return on that single stock is greater than a standard index position. Despite my general belief in the ‘laziness’ of passive index investing, it is far more straight forward if alternative clear choices are not forthcoming.

Download the current Portfolio#1

Thanks for reading in 2025 and Happy Investing!