The HindeSight Letter

ISSUE 122 - April 2025

OVERVIEW

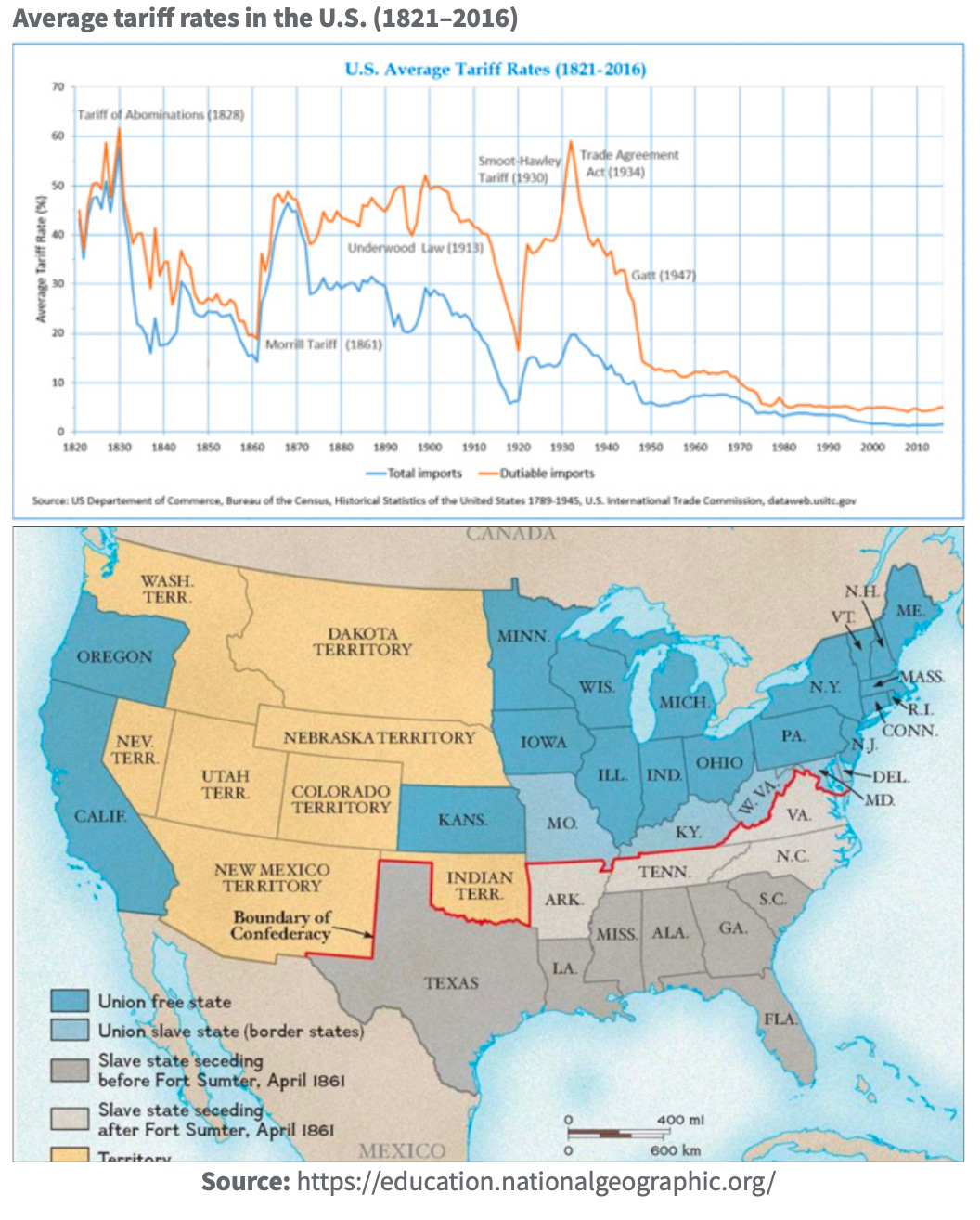

The early 19th Century saw the young US federal government impose a series of tariffs beginning in 1816. The War of 1812 and Napoleonic wars had seen British manufacturers offering goods to America at low prices as a result of the European blockades which US manufacturers found difficult to match. Tariffs were seen as a protection for the newly developing industries in the US and a revenue generator. However, the southern states were fiercely opposed as the economics were sharply divided between the industrialising north and Union states and the agriculture based economies of the south, leading to the 1828 tariff being known as the “Tariff of Abominations” at 38% on certain goods. It would be another 30 years until the US Civil War would commence and historians have long debated all the causes of that tragic conflict apart from the much-accepted belief of slavery use and expansion but the issue of federal and state authority and power that still exists today, stems from these early days of the New World.

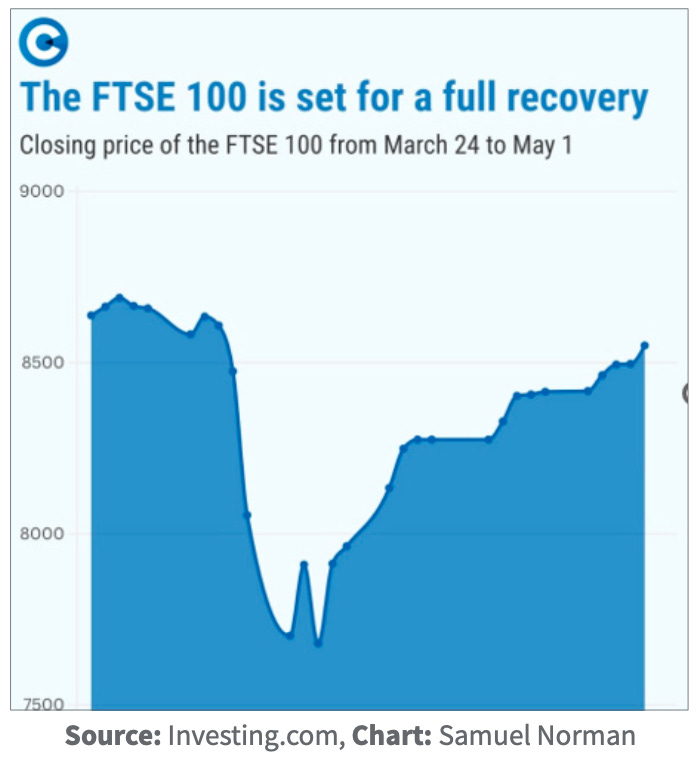

One of the benefits of writing a monthly newsletter is being able to have more time to understand and assess the effects of events during that time. In this case, it is almost a month since the “ Trump Tariff Madness” saw stock markets plunge all over the world. The FTSE 100 Index that hit a high in early March above 8900 dropped over15% in a few days to a low of 7533 on April 7th with the rest of global markets echoing that fall. Yet, just a few weeks on, the markets have almost recouped all their losses with the FTSE enjoying its longest winning streak in history, with 15 consecutive positive days at the time of writing. Have tariffs been forgotten or has all the incredible negative press being “fake news” or have the markets decided that tariffs aren’t so terrible after all and the narrative moves on?

It’s difficult to truly like US President Trump even if you see some “method in the madness”. The arrogance and lack of empathy in most of his comments often over shadows much of his 100 days of Executive Orders. Whether I live in the US or Europe, I am hugely in favour of reducing the size of the state largesse with its obvious waste and inefficiency. Likewise, I am naturally far more supportive of meritocracy than diversity and equality process in any employment environment. The issue of unplanned immigration is always contentious but the deportation of immigrants that have committed crimes should be so obviously accepted, it should be a non-issue. These make up much of the Executive Orders as well as the concept of “equalising” policies in President Trump’s mind. Whether it is forcing European NATO countries to pay their fair share rather than freeload off the US or addressing the huge trade deficits with supplier countries, there is some structured thought, despite the delivery.

The hatred and denigration of Trump’s tariff policies in the media has clearly been overdone which is probably what the markets have grasped. Of course, you won’t find a single economist that believes there is any merit in tariffs as well-thought out protectionist and trade policies but from the reactions of a few weeks ago, you would think this is the first time in history that anyone has ever imposed tariffs. But, of course tariffs have been around forever in some shape or form but in the US apart from possibly some factor for the US Civil War, the only real reference point that economists and historians have is the Smoot-Hawley Tariff Act in 1930. The accepted analogy was that it directly contributed to the Great Depression of the 30’s with the decline in trade.

Tariffs were the primary tax revenue for the early US and British governments. On the eve of the US Civil War in 1861, 90% of federal tax collection and funding was from tariffs. As excise duties were brought in, typically on alcohol and tobacco and the early income tax policies, the reliance on tariffs declined but for the ordinary worker, income taxes didn’t affect them until 1913. Nowadays, you will still see emerging countries with high tariffs and import duties, 10-30%. Look at India which up till the UK trade deal yesterday had 150% tariff, now 75% on all whisky and gin imports. This simple tariff tax collection serves a vital purpose on countries where the structure for income tax collection isn’t up to scratch yet. Most of the large developed countries tend to have much lower tariff rates but where they exist, they often still serve the origin purpose of tax collection and trying to protect home industries, as exists between Europe and US.

God knows what the total tax extraction is in the UK on the average worker between income tax, excise tax, VAT et al, but I imagine it’s at least 50% of total earnings, all to fund our huge state enterprise-think civil servants Defined Benefit pensions! So it’s interesting to hear Trump mention that US can make so much out of tariffs that he can reduce income tax for the lower paid workers. If that isn’t a vote winner, I don’t what is, but are the maths even close on that.

Last year, the US imported $9bn worth of goods every day, totalling $3.285 trillion. If it was as simple as getting 20% on top of that as tariff collection, so $657bn, this would be theoretically possible, Total tax collection in the US last year was $4.5 trillion, roughly half of that from income taxes so the $657bn might indeed be relevant, if actually obtainable.

Of course, it’s not that straight forward. Economics 101 says with higher prices, demand drops and you get nowhere near that tax collection number and there are loads of other obstacles to overcome not least for the US as the world’s reserve currency, the Balance of Payments equation of;

Current Account + Financial (Capital) account = 0

Here is a link to an excellent piece from Ben Davies, my long-term friend and old partner at Hinde Capital who explains it far better than I could.

www.linkedin.com/pulse/death-dollar-diplomacy-ben- davies-abxte

The essence is;

The Bretton Woods II system hinges on a loop:

Surplus nations export goods to the U.S.

The U.S. pays in dollars

Those dollars are recycled into U.S. Treasuries

Trump's tariffs short-circuited this loop:

Less trade means fewer dollars go to surplus countries.

Fewer dollars mean less recycling into Treasuries.

The cost of U.S. deficit financing goes up, just as debt issuance explodes.