HindeSight Letters Investment Insights Archive - READ HERE

Our FREE archive posts allow our subscribers to access valuable insights and analysis and a deeper understanding of market trends and investment strategies that were relevant at the time the HindeSight newsletter was published.

Additionally, reading archived newsletter content can give you a sense of the long term performance of the investments or strategies discussed which can be helpful in making informed investment decisions.

Furthermore reading this content can provide historical context and help you see how market conditions have changed over time, allowing you to better anticipate future developments.

Overall reading our archived content can be a useful tool for gaining a broader perspective on the market.

LIMITED OFFER. GET A 90 DAY FREE TRIAL OF OUR PREMIUM SUBSCRIPTION & MAXIMISE YOUR INVESTMENT POTENTIAL

INVESTMENT INSIGHTS

Originally posted in July 2015

‘A State Secret’ By Ben Davies

The gambling psyche of the Chinese has driven its economic miracle of the past few decades. Far from State Capitalism engaging in thoughtful planning, it has lurched haphazardly and reactively from one policy decision to another. We are not witnessing true reform in China to foster open democracy, instead the policymakers are merely restraining elitist groups and seeking to solidify the central power base.

The liberalisation of stock markets has been a policy gamble to arrest their debt-ridden economy, whereby they have recklessly encouraged a transfer of (more) risk from SOEs (large state-owned enterprises) to their population. Their poor beleaguered people cannot grasp the magnitude of the deception. They are so addicted to their own need to gamble, the recent stock mania and crash has only compounded to seal their economic fate.

The situation in China highlights the continued global struggle between the State and individual rights. How ironic that the command economy should fail at the hands of an open stock market (of sorts), when the West shifts ever further towards the closing of markets and State capitalism, so associated with such a command economy.

The largest debt-for-equity swap in history has failed. The question is, are we now all in it together or not?

A little State secret: the State can't control the economy and markets at its will. At some point the system fails to work properly, destroying any wealth created. Such wealth is merely an illusion – mere vapour.

Deng Xiaoping was once reputed to have said, "Some people insist stock is the product of capitalism. We conducted some experiments on stocks in Shanghai and Shenzhen, and the result has proven a success. Therefore, certain aspects of capitalism can be adopted by socialism. We should not be worried about making mistakes. We can close it [the stock exchange] and re-open it later. Nothing is 100% perfect."

It is clear that the Chinese authorities took his advice at face value. In recent weeks, the mania in the markets has begun to turn to panic and the authorities suspended over half of all stocks on the exchanges on July 7th and 8th. At one point, even the companies themselves requested their stocks be suspended because bank covenants had been breached, as they had pledged their own stock as collateral for bank loans.

This truly unprecedented behaviour was just part of a list of extraordinary measures undertaken by the mighty ruling party. I list a few here. The PBOC implemented a rate cut and RRR reduction, whilst brokerages, fund managers and insurers were instructed to buy even more stocks. The liquidity came via a direct line of credit from the PBOC to the China Securities Finance Corporation (CSFC), a provider of margin financing who would then guarantee ample financing for all of brokerages. CSFC by the way is an SOE no less!

The China Securities Regulatory Commission (CRSC) ordered companies to buy back 20% of all the stock they had issued in the past six months. The Insurance regulator (CIRC) increased the equity allocation back from 30% to 40% (which it had only just reduced the week before) and doubled single-stock holding limits from 5% to 10% for good measure as well.

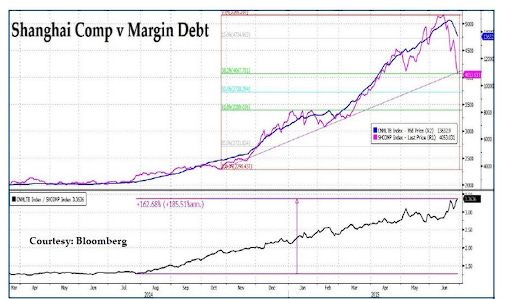

One of the best quotes on recent events I saw, was from Goldman Sach's China Strategist Kinger Lau, who said: "Leveraged positions aren't big enough to trigger a market collapse... it's not a bubble yet... China's government has a lot of tools to support the market." Is this gentleman completely nuts. He certainly must be a loyal citizen and one of the cadre. If peak financing of $355bn or 12% of the value of all freely traded shares on the market (which is apparently the largest ever recorded in financial market history) then I would say Lau has been smokin' too much of the Shanghai opium pipe of old.

Sean Corrigan did some further great analysis on margin, which he presented in ‘MidWeek Macro Musings’ (a publication that comprises of about 7 to 9 pages each time with really insightful charts on money, macro and markets) alongside a pithy explanation. In the 8th July weekly, Sean wrote that at the peak of the market, the margin (if you include the shadow as well as official margin debt) would have been at a staggering 25%. The 12% was the official margin debt.

The shadow margin was flourishing in the P2P sector:

“Nor have they yet gotten to grips with the many-headed hydra which is the nation’s flourishing internet-based P2P network, a teeming ecosystem which counted over 1700 members at the last reckoning at the end of 2014 but which is probably even more populous now that the demand for funding has become so unstoppable. The interaction between firms, individuals and the banks and other financial intermediaries who come between them has become so profuse as to leave one dizzy. As Tencent laid out in a lengthy article on the topic, whether on the TV or internet, in the press or on stationary advertising hoardings, it is currently impossible to avoid the ubiquitous advertisements for sources of margin finance. ‘We provide the funds – you keep all the profit’, as one of the more prominent temptingly declares. Needless to say, the contractual terms of such arrangements are carefully drafted so as to evade any regulatory restrictions, including the ostensible (but fundamentally non-existent) separation of the funds’ providers from the intermediary offering the ‘service’.”

The extent of the impact on the wider economy has been for all companies to reallocate their dwindling capital to this new mania and ‘The Economist’ thinks this crash will have no impact on the broader economy! Sean:

“To take a different example, smartphone manufacturer Xia-omi has recently launched a consumer finance arm which is to be expanded into an asset management company. Meanwhile, companies in languishing sectors, such as steel manufacture, electricity distribution, coal mining, and real estate, are said to be particularly active in redeploying their capital – and, no doubt in making avail of their credit lines – to reap the rewards not just of stock speculation per se, but also to profit from the usurious fees and interest charges – often amounting to several percentage points per day – to be had by funding the punting classes.”

Early on, I highlighted the extent of China's gambling addiction. When we bear this in mind, we may begin to question the decision-making of the ruling party this past few decades. We may begin to look at those decisions in a new light. So China, far from being some sophisticated, well-controlled command economy, has just been one chaotic gamble after another; a juggling of the mahjong pieces to keep the Chinese economic juggernaut moving forward.

The 5-year and 20-year plans we have read off so much of in the China Communist Plenums seemed to point to such a certainty of direction. They were so seemingly assured of their outcomes. But surely, those who cheered the might of Mao's descendants must be really beginning to question whether the State really has omnipotence to manage the levers of its economy?

I have read in ‘The Economist; recently that the Chinese ran and marshalled the economy well. This is plainly ridiculous. There has certainly been a semblance of growth and stability, but this is now unravelling and instead of restructuring the equivalent of 225% to 250% debt to GDP (which is likely to be far worse when the murky world of WMPs and LGFV is fully accounted for), they have chosen to shift the risk onto Auntie and Granny in a stock market bubble.

It's clear that years of State intervention have built up consequences which are being exposed with magnifying proportions as they attempt to shift risk from closed, less liquid and frankly completely opaque parts of the economic balance sheet to the relative transparency of the open capital markets. (I say 'relative' transparency, for let’s be under no illusion, there is no central body of gilded governance and accountancy consistency among these listed companies).

It seems that the talk of market liberalisation, whilst telegraphed, has begun to be undertaken out of desperation to arrest the collapse of its economy at the hands of ailing balance sheets. Pulling a tiger out of the proverbial hat may seem somewhat easier than transitioning China to a more open-market economy when its country is swimming the tide of quicksand, as its debt sucks in all round it. And as I have warned, sucking the rest of the world in with it.

‘The Economist’ patently miscomprehends what the Chinese have been doing here. By trying to save the economy with a vast debt-for-equity swap, they have merely succeeded in creating an even more highly geared economy whereby illgotten equity gains were being redistributed into other sectors, such as Real Estate, the very asset that has been at the centre of the over-reaching economy.

Xia Dan, an analyst with Bank of Communications Co, summed it up nicely when he told a reporter that: “There is a renewed enthusiasm about buying real estate, which stimulated a rise in both sales and prices. The bullish stock market has generated massive wealth, strengthening a willingness to buy houses... Momentum in first-tier cities is particularly strong.”

And as Sean pointed out:

“As has been the case in every great financial mania since the days of John Law, each element of the madness is now fuelling the other. The NBS itself admitted that no less than 97% of the minor improvement in the April profit numbers for ‘above-scale enterprises’ was due to gains realised on firms’ stock investments, not to any brightening of operational conditions. With UOB Kay Hian economist Zhu Chaoping calculating that such entities’ notional holdings had doubled in a year to just shy of CNY1 trillion, there must seem plenty of scope for more of the same.”

The fall-out of a failed attempt to revive the economy through this latest gambling directive by the ruling party, far from having little impact on the economy will most likely accelerate their deflating economy. ‘The Economist’ wrote that because stocks account for only 15% of household assets, the stock market crash will have little impact on consumption. This misses the point entirely. It is the investment spending boom which has driven the economy this past few decades and it is this which is now even more levered and fragile, as despite stock markets being up 75% or more since the bottom, loans and investment decisions had been taken out/on with values substantially higher than here. And whilst we will have a momentary reprieve in the markets with a State induced bounce, it will be a dead cat bounce as companies and investors take any opportunity they can to offload their losing positions.

The risks in China are so similar to the sub-prime crisis with Real Estate risk at the epicentre of the problems.

I would add though, in contrast, that in the annals of this history this market movement may well look like a flat line in the upward trajectory of a stock market. For at some point, China will build a US-styled 401k deeply liquid capital markets in both debt and equity to satisfy Chinese wealth and savings via a growing pension fund industry. If you look at the 1950s to 2015 in the US stock markets you will get the picture, but this assumes a big ask. Will China establish the yuan as the global monetary standard supported by a large military complex as have the US? For that is what must happen for this trajectory to potentially occur, although 1 billion active investors could be a very powerful dynamic, aging demographics aside.

Unfortunately, this recent opening of the stock markets (the HK-SH connect) wasn't about reform. This was a last-ditch move to shift the risk dynamics of the economy and when it didn't work the authorities panicked and shut down the roulette table. The losses are too big. The next step is surely to just socialise and restructure all the local government and SOE debts, but this will then threaten the power base of the regions, something the ruling party doesn't readily meddle in.

Take It On The CHINext

So fast has the mania and crash been, it is faster than anything that has preceded it in history. The duration, and hence velocity, of the crash has been so swift that the editors of Kindleberger's M’ania, Panics and Crashes: A History of Financial Crises’, may well have already written the first and last draft about this astounding event already. The chapter should tell 'how gambling was so endemic in China that it was only a matter of time before China's cultural crowd of speculators from the authorities to Auntie would turn into a deranged and maddening crowd fuelling stocks to an average value of 147x earnings. The subsequent crash would put the final nail in the coffin of a collapsing economic superboom.'

As with any mania there is always the "new, new thing", as Michael Lewis once wrote. Sean picked up on this notion when he wrote:

“Much of the focus of the wider ’investing’ public is, as ever, on ’concept stocks’, whether internet-related, telecommunications, or so-called ‘cleantech’ in this incarnation. Partly, this is because these are the ones being talked up by the regime as offering the pathway to a brighter, more prosperous future now that the smokestack days are fast fading into oblivion. Partly, however, such New Era counters are prominent because a sizeable proportion of the new stock market gamblers are students – some, moaned one dis-gruntled professor to Xinhua, devoting up to six hours a day to ‘researching’ and trading their plays instead of studying to master their disciplines. How very non-Confucian!

“As we have also seen, many such companies are them-selves benefitting from providing the financial and informational infrastructure bubble. Thus, for so long as it lasts, they are able to produce a simulacrum of earnings growth and hence are seemingly able to validate some of their student sponsors’ bullish prognostications.”

The extent of Premier Li Keqiang's gamble had even extended to a personal endorsement of Beijing's third OTC board, whereas with any good mania the IPO market exploded. In China, the State controlled the pricing of IPOs, not the market. They were held at artificially lower prices and then let loose on the market. The number of listed firms skyrocketed from 2013’s 343 (combined market capitalisation of CNY137bln) to May 2015’s 2,486 (market cap CNY850bln). So far, June has seen a further 114 new members, projecting a year end total in excess of 4,000...

“...the regime which, desperate to keep the plates spinning using any and all means, has already announced that not only is it looking at relaxing (!) rules for IPOs and at providing NEEQ (as is the Third Board’s official designation) entities with an easier exit onto the slightly less Wild West uplands of the ChiNext NASDAQ analogue, but that it will set up a ‘Strategic Emerging Industries Board’ at the Shanghai Stock Exchange in order to ‘attract private capital in emerging and creative businesses, and provide an exit channel for private equity and venture capital investors’.”

Saving Face

Addicted to their own mianzi (face), Chinese officials would far rather deny that problems exist than deal with them. I believe their gambling mentality and inability to recognise when they are wrong has maintained a charade of economic posterity.

President Xi Jinping referred to the slowing Chinese economy as the 'new normal' after years of double-digit growth. The arrival of the AIIB to help fund the new Silk Road projects has come at a convenient time. Whatever any economist says, China is still not shifting away from a country blighted by over investment in infrastructure building to grow its economy.

There is nothing new about how the Chinese are behaving. When I saw the Bloomberg headline on the morning of the 8th July – that they had banned stock trading – I just laughed with incredulity. I thought why not just suspend them all! Don't do half measures. At least that way you can guarantee they won’t fall. Now all those overseas investors who participated in the market are locked in, as the ban is in place for over 6 months. As a colleague quipped, it's like hedge funds gating their funds in 2008 – the Chinese stock market is now just one big closed hedge fund. I must say that the legendary investor Stan Druckenmiller’s comments on ChiNext being a sign of a recovering China economy are proving to be very, very wide of the mark. I couldn't have disagreed with him more at the time. Like ‘The Economist’, I believe he has missed the bigger picture we have discussed here.

This whole debacle has been about herding the collective to arrest medium term outcomes. It is a fallacy that China can stymie the impacts of market forces even within a socialised form of capitalism (State Capitalism). Of course, evidence would appear contrary – in the past the State has had the firepower to bail out banks. Think 1999, when Asset managers were used to bail them out at behest of government and then of course the famous floating of the banks to recapitalise them in 2003.

Think about how the State set up a stimulus program in 2008, as mentioned earlier, which saw excessive bank lending to SOEs and Local Governments (LGFVs) to fund white elephant infrastructure and industrial projects. Think of all those new SOEs that were formed to take advantage of this cheap credit, as private companies were not included in the mandate. But like with most emerging economies, what tends to be the one most important driver of economic success? It is housing and a booming real estate market which has been the sole basis for a massive expansion of credit and supply of capital in such countries. In China specifically, this helped fund all these local govt infrastructure and industrial projects. Again, it looked like the State could control outcomes.

It’s the local governments who own the “LOCAL” or agricultural land. The State has tried to control the real estate bubble and it looked like it was taking the heat out of it carefully, but in reality it has been the local governments and SOEs who have a stranglehold on local land prices and prevented a complete rout. They have controlled what could be sold. Even though projects were technically insolvent they have been able to supply enough capital by selling off small parcels of land at sky high prices and thus borrow again based on this scarce market value. As in reality, if the market was freed of such influence prices would plummet with all the supply available. But as we all know, it appears now that the Local Government (LG) are now just selling land from one LGFC to another, so it’s a game of musical chairs or pass the parcel. It has an end game and it’s an exploding parcel for those local governments and by dint China.

Yet it is also true that the central state doesn’t get involved in LG budget affairs. There is talk of property taxes and enforced selling of wasteful assets accompanied with LG fiscal budget limits. But if this does happen civilian unrest is likely. I also read that there is talk of the State allowing LGs to issue bonds to pay off their existing debts, which is effectively what happened in the 90s and was never paid back. Remember, the plan of late 2013 to allow mixed ownership of SOEs, where private companies could hold a minority stake in SOEs? That has been disastrous as it just widened their (SOE) asset base and postponed the inevitable – cue stock market mania and panic.

It seems the reforms of the past two decades occurred because it didn’t upset the applecart, it enriched people – now reforms attack the status quo and vested interests. (I repeat, it seems to me that reform now is less about open democracy and more about controlling the China “resource” barons and debt implosion). These SOEs have a good thing going and have a judicial advantage relative to private enterprises. Just as in Japan in the 80s, even to the present day, these collective interests are crowding out true efficient deployment of capital by the private sector. They have helped to maintain the charade but it is clear it is unravelling and other than full socialisation of losses, the State is powerless to prevent or lock in the losses.

Of course, under the guise of “liberalisation” we have this HK_SH connect and an “open” stock market. Well the State found it can’t control this either. The difference with an open market place which has instant liquidity, as opposed to the glacial illiquid housing market, is there for all to see, plain as day. The State can’t mask the realities that half these companies don’t actually exist. Take ChiNext. The stock market is not a barometer of the economy as Druckenmiller suggests. It has been a nationalist encouraged version of Mahjong and Sic Bo on the grandest of stages. No amount of enabling and then disabling stock account openings and margin levels going forward can alter this fact.

The Chinese market has seen consistent speculative failure over the years – you can’t say it’s a fledgling market any more. Corporate governance and sound accounting practise (or audits of) is sorely missing though and yet it’s still not young in duration.

The question that we must ask ourselves – and I will leave you all to ponder it – is this, does the failure of the Chinese authorities to manage their stock market reflect the realities that even in the developed world stock markets cannot be underpinned by QE and intervention indeterminably?

Now the Western markets may not have the excesses in individual margining (we can debate) and silly valuations (although median values are high) as China, but there is clearly high credit, high margin exposure in Western equities. We have begun to all believe markets can be held up by the Central Banks/ State – we have conditioned ourselves to a 'don’t fight it mentality'.

So unless by some miracle China can build the market to new highs in the next few years, the fall-out on the Chinese economy will continue. This is just another sign that interventions to maintain the Bretton Woods II monetary system cannot continue.

Of course, we all want to believe that the status quo is more likely, that the world continues to limp along for decades and that it's even possible that the immense technological innovation we have witnessed to date in such a parabolic fashion will erode the debt bubble and maintain nominal GDP levels. That there will be no conflict between aging demographics and robot workers, such will be the productivity gains. But this is clearly not a given and so a much larger debate to be solved for another time.

I can see decades of debt eroding, but without visually higher CPI prices our collective debt is still rising. Asset inflation can alter the net debt calculus – if assets rise to such a point that interest expense cannot be met by cash flows, then prices will fall and debt to equity metrics will once again become problematic. We are clearly on the cusp of this with markets rallying and then failing. The parcel is being passed, the only question is – can we find new players to pass it to? Are we truly "One for All and All for One''? The State secret says otherwise.

Sector Returns

The smaller companies of the FTSE 250 continue to rise as a % of the FTSE 100, often reflecting very late cycle dynamics, despite Greece and China. In fact, the large caps have suffered disproportionally to their smaller counterparts, although this is understandable in the basic materials and energy sectors as commodity prices slump even further.

WHY CHOOSE US?

HindeSight Letters is a unique blend of financial market professionals – investment managers, analysts and a financial editorial team of notable pedigree giving you insights that never usually make it off the trading floor.

We help our paid subscribers have 100% control to build their own portfolios with knowledge that lasts a lifetime and all for the price of a good coffee a month - just £4.99 or save 2 months by subscribing to our yearly plan, only £49.99.

Our history is there for all to see, measure and research.

LIMITED OFFER. GET A 90 DAY FREE TRIAL OF OUR PREMIUM SUBSCRIPTION & MAXIMISE YOUR INVESTMENT POTENTIAL

Visit hindesightletters.com for more information