HindeSight Letters Investment Insights Archive - READ HERE

Our new archive posts allow our subscribers to access valuable insights and analysis and a deeper understanding of market trends and investment strategies that were relevant at the time the HindeSight newsletter was published.

Additionally, reading archived newsletter content can give you a sense of the long term performance of the investments or strategies discussed which can be helpful in making informed investment decisions.

Furthermore reading this content can provide historical context and help you see how market conditions have changed over time, allowing you to better anticipate future developments.

Overall reading our archived content can be a useful tool for gaining a broader perspective on the market.

INVESTMENT INSIGHTS ARCHIVE

Originally posted in January 2016

If you had recently typed in stock market and panic into a search engine, you’d have found multiple articles, mostly of the ‘3 reasons not to panic about stock market declines’ variety. As every investor knows, as stocks in the long term will always go up as a general rule, it makes obvious sense to always buy on dips, the bigger the better. Unfortunately, the reason why this has been the case is less well understood.

If we glance at the last few decades in the US and European stock markets, you can see the general trend upwards. While we have had a few nasty drawdowns in 2001 and 2008, and the FTSE 100 and French CAC have not risen to the highs of the US SP500, DAX or FTSE 250, the investors’ buy on dip mentality and long-term hold seems to do well. So that’s settled then?

However, in my opinion, the reasons that can be attributed to these gains lie with factors that may be difficult to continue to replicate in the future:

• A continual decline of interest rates, making the cost of capital and debt servicing lower

• A continual increase in debt; sovereign, corporate and personal

• A high rate of growth in the global population, not just an increase in population

• A large, strong workforce that is generating productivity gains

• Global emerging growth, which is often commodity related and bringing in capital inflow (Foreign wealth)

• And recently, the extraordinary monetary policy of central bank balance sheet expansion

Currently, the most concerning situation in the world of interconnected global finance is the ‘beggar thy neighbour’ currency devaluation policies, coupled with the drastic decline in the price of oil that looks more permanent than in the past.

Most world currencies are losing value against the all mighty US dollar. Any hope of gaining export growth by currency weakness is muted if everyone is playing the same game.

Oil producing countries are using up their monetary reserves as their budgets weaken and they try to defend their currencies in vain. Russian looks particularly vulnerable. A comment today by a Russian journalist in response to the question was:

“How are things? Pretty bad. Devaluation has impoverished the population, wages are 2-3 times lower than 2013 in USD terms. The 2016 budget was constructed with 3% deficit and oil price of $50 per barrel. When oil was $100, about $70 went to the budget, about $35 export duty and $35 mineral resources extraction tax. At $30, we have a very big problem. Our options are to devalue further, tax more, spend Reserve fund, privatise something, or a mix of all. The banking system is the other problem. Second tier banks are collapsing now. We have circa 600 banks and in the top- 100 we have alarming bankruptcies. At Vneshprombank, for example, top-34 (rated by Moody’s and S&P), assets of roughly $4bn were totally stolen. This is a widespread problem with falsified accounting. Personally, I think that the assets of the bigger and biggest banks are not much better. Nabiullina (head of the Central Bank) is trying to do its best, but the system is totally rotten.”

If anyone needs a refresher course in Russia and the business problems there, Bill Browder’s new book ‘Red Notice’ is an excellent but worrying read. By coincidence, I was last in Russia during the winter of 1991 when there was a real crisis going on as well. I spent 3 weeks there with my Russian tutor and for many days was not able to buy food. The best diet plan ever. Twenty-five years later and Russia, after enjoying a capitalist boom almost unparalleled in history, has returned to Earth with a resounding thud. I understand the current import/export sanctions are having the same shortage effect as 1991 and any traveller to Russia may only take 5kg of non-Russian food with them.

If China continues to devalue their currency, with some arguing for up to a 50% drop in the Yuan, how will the world cope with that deflationary export?

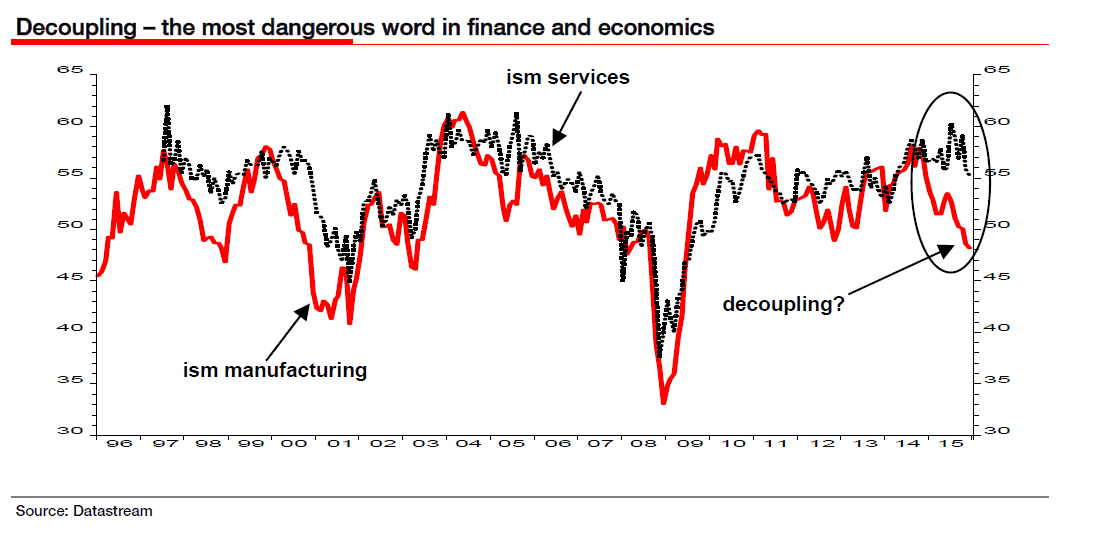

The US dollar’s strength is not an ideal way to benefit US exporters and Albert Edwards of SG and our own Sean Corrigan show us their thoughts on that below.

The US institution of supply manufacturing index and the US institution of supply services index, both looking unhealthy.

My belief is that we are fast approaching the event horizon of a potential financial black hole that will make 2008’s GFC seem immaterial. I hope I am wrong, as I certainly don’t relish all the other far-reaching effects of a true crisis, as it won’t be just about rich people losing money.

It would be hard to argue that the factors I have listed above have had no impact on the level of global assets in the recent 4 decades, and as such we must worry that it will be almost impossible to continue.

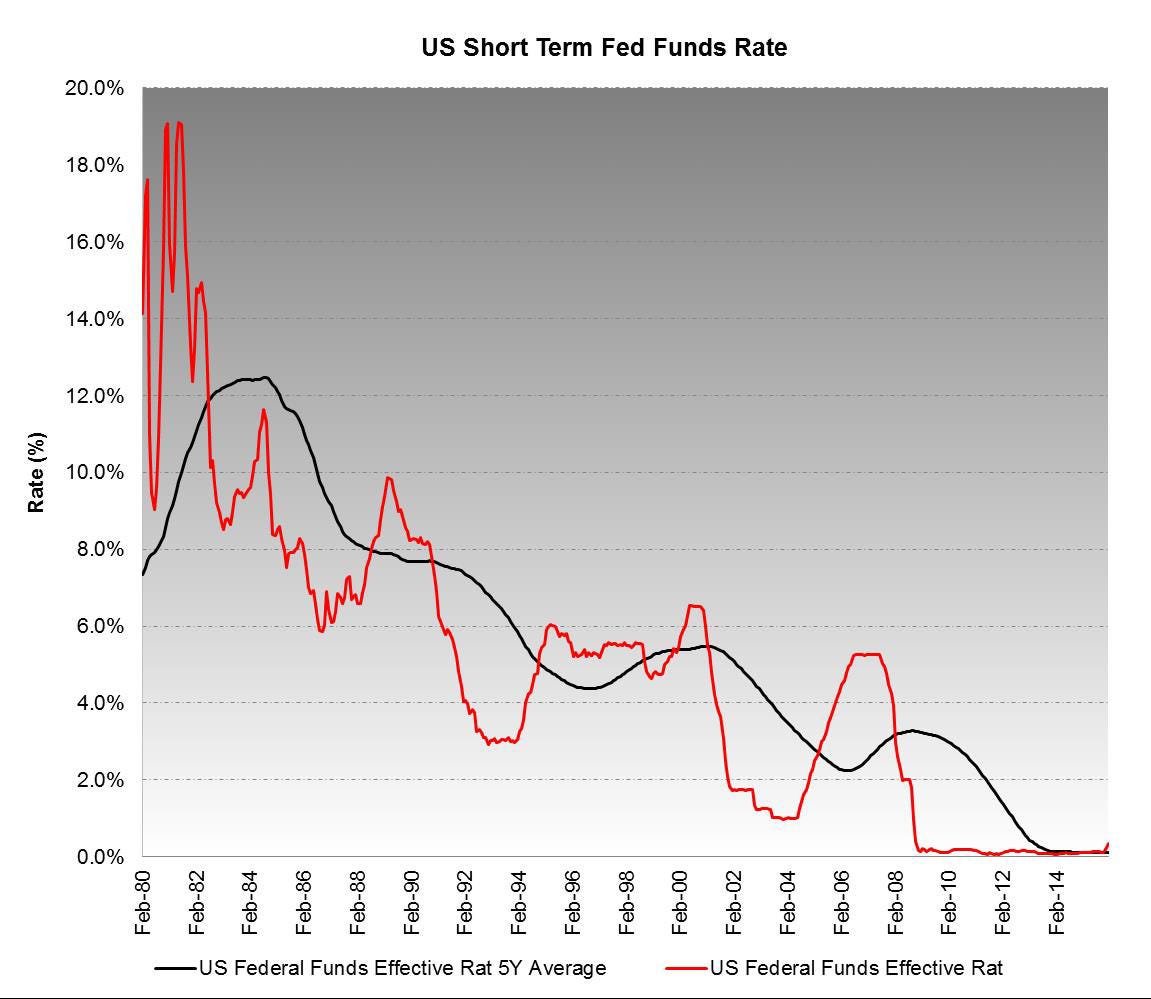

• With interest rates at zero or slightly negative in many countries, the belief that the central banks can continue to lower them in order to force consumers to spend surely hits a wall, as negative rates are in effect a tax and higher taxes rarely help consumption

• Running budget deficits at every level of society forces indebtedness, where we borrow from our future earnings. Surely there is a limit here as well

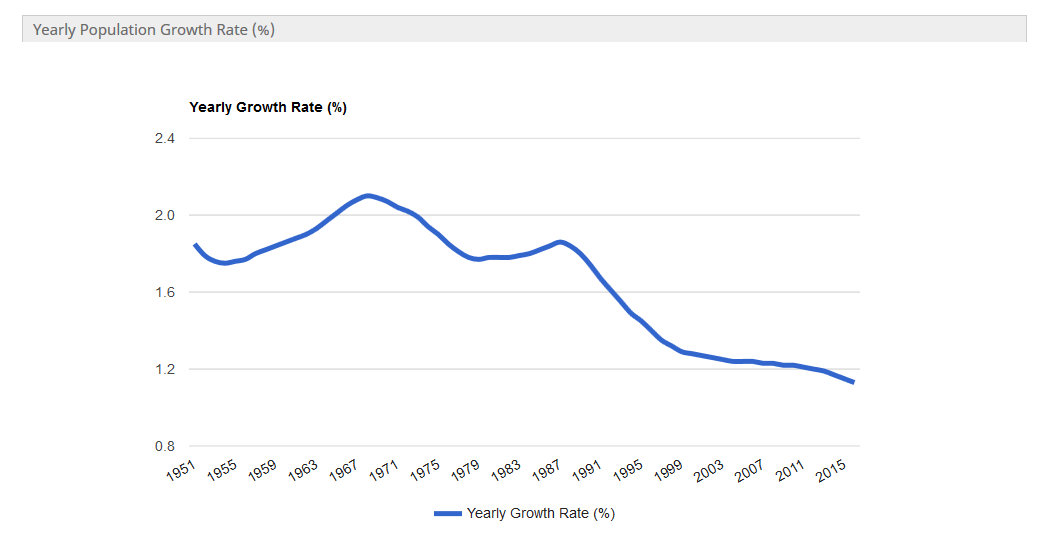

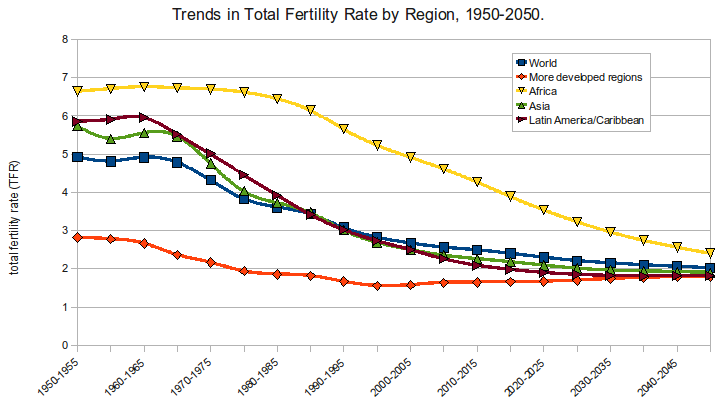

• While the global population is still growing, the rate of growth is falling fast with many countries fertility rate far below the necessary 2.1 replacement rate. Many populations from Japan, Germany, Russian and even China will decline in the foreseeable future. Even more worrying is the even more dramatic declines that are expected in the workforce as demographics play their hand. Instead of earning, spending and saving, you just get a drawdown of the savings

• The rich foreigners have often brought wealth from overseas. Places like London have benefitted tremendously from the nouveau riche of the day, from the Middle East, the Russians and the Chinese, as well as the Americas. Who will replace this void in the London housing market now that most are experiencing a domestic crisis

• In theory, extraordinary monetary policy and balance sheet money printing expansion by central banks is limitless, but history has told us that this leads ultimately to a complete currency and system reset

With all these concerns, it would help if valuations of stock markets were relatively low and discounted future worries, but sadly they are at exceptionally high levels wherever you look. If we look at the price multiples of the developed stock markets, you find a general range of forward Price/Earnings in the 16-20 times, far above historical averages. Let us remember what that means in layman’s terms. If you buy an asset at 18 times earnings multiple, you have to wait 18 years just to get your money back. Can growth illusion really justify that for the whole of the stock market on average? The fact that profit margins look set to fall suggests that not only is the price/earnings multiple very high, but future earnings are potentially at risk too.

Strangely, we have had a potential preview for how this may play out, namely Japan since 1989, when valuations hit sky-high levels. Since then we have seen rate cuts, QE balance sheet expansion, no inflation, no growth and a declining population. From the highs of 1989, the Japanese Nikkei equity index dropped by as much as 80%, before doubling off the lows and oscillating between down 80% and down 50% for the last 26 years.

So when you next read ‘don’t panic, buy dips in stocks for the long term’, pull out the Nikkei chart and wonder if you will be alive that far in the future.

I want to end on an optimistic note. IF asset prices, like property and equities, collapse amid currency chaos, it’s very possible that the main beneficiary of this crisis will be the youth. The youth who currently can’t get on the housing market or are forced to save into overpriced equities, if they save at all, will be better off as long as they can keep employed. The working youth deserve a new start at the expense of the older, rentier class.

WHY CHOOSE US?

HindeSight Letters is a unique blend of financial market professionals – investment managers, analysts and a financial editorial team of notable pedigree giving you insights that never usually make it off the trading floor.

We help our paid subscribers have 100% control to build their own portfolios with knowledge that lasts a lifetime and all for the price of a good coffee a month - just £4.99 or save 2 months by subscribing to our yearly plan, only £49.99.

Our history is there for all to see, measure and research.

Visit hindesightletters.com for more information