HindeSight Letters Investment Insights Archive - READ HERE

Our new archive posts allow our subscribers to access valuable insights and analysis and a deeper understanding of market trends and investment strategies that were relevant at the time the HindeSight newsletter was published.

Additionally, reading archived newsletter content can give you a sense of the long term performance of the investments or strategies discussed which can be helpful in making informed investment decisions.

Furthermore reading this content can provide historical context and help you see how market conditions have changed over time, allowing you to better anticipate future developments.

Overall reading our archived content can be a useful tool for gaining a broader perspective on the market.

INVESTMENT INSIGHTS ARCHIVE

Originally posted in July 2018

I recently had the pleasure of catching up with an old American ex-colleague and friend for dinner. In the late 90s, we worked together in the US government bond market world with much higher interest rates and volatility, aka ‘the fun times’.

He now runs a large fund, investing capital with small to medium businesses all over the world. His fund looks for businesses that provide two basic fundamentals:

• An ability to generate earnings from a positive margin

• Having good assets that can be used as collateral

It doesn’t seem too much to ask if you are a company looking for capital, either to see you over an unforeseen business problem or to assist in growth development. My only question to him was, “You must be in pretty intense competition? People seem willing to throw money at anything these days.” The answer strangely was ‘no’. Real business is out of fashion, apparently.

The huge money waves of investment capital seem to only be interested in growth at any price, companies that don’t make any money at the moment, but with exponential growth rates that are funded by regular equity financings which ‘will’ be hugely profitable in the future. Of course, some of these companies will do just that. The world is changing and disruptive companies with a better business plan may well be able to grab market share and become profitable, not just by providing an amazing service to customers (think Spotify, Uber etc.), but also by providing returns to their shareholders. But some – maybe many – will not.

Take WeWork, the co-working space provider. Currently valued at $20bn, it managed to put in a $1bn loss last year, while raising $2bn from investors to ‘keep growing’. It expects to need another $2bn next year. WeWork’s business plan to date has been to take on long-term leases from existing landlords, put in ‘break-out areas’, free coffee and beer, and reduce the desk workspace from 200 square feet per person to 60. In theory, it is ideal for start-ups who want the illusion of working in a proper office but need a very short rent liability as a high percentage of them fail in the first year.

It is, in effect, property arbitrage, cramming more people into the same space that the offices were originally intended for. (Think HMO, houses with multiple occupancy). But, it’s a business plan that is currently receiving a lot of interest. It’s not clear to me at all why IWG, the old Regus. who have ten times the office space is valued at a sixth of WeWork, but that’s marketing and trumpet blowing for you. We have used Regus and WeWork ourselves for businesses in the last twenty years, and on both occasions, when our business felt able to stand on its own two feet, we took on normal city leases rather than be so incredibly close to each other. Personal hygiene became a major talking point, and if that was my fancy, I can always get that on the Tube in the midsummer morning rush hour!

The worry with any valuation, and not just with a $20bn one, is that if everyone leaves WeWork after their business takes off or fails, the company’s rental income hardly seems to be on a solid footing. Certainly, when we rented a small ‘eight’ man office at WeWork, we didn’t come across too many pawnbrokers, DIY businesses or doctors’ surgeries in there paying the rent. How many recession proofed businesses will be left when – not if – the next downturn comes? Meanwhile, WeWork has huge long term leasehold liabilities, but hey, as long as the economic expansion keeps going and cheap equity financing keeps coming, all’s well.

It seems a far cry from my friend’s business. In previous financial shocks, history tells us that access to cash and financing dries up pretty quickly and businesses have to survive on their earnings alone. They have to manage huge liabilities very tightly or bankruptcy looms quickly. There are many new entities out there that are going to learn this lesson in the future. Far too many, in fact, to make it through even a small downturn unscathed.

PORTFOLIO THOUGHTS

In the summer of 2008, in the depths of the Great Financial Crisis, a lady came to us at Hinde Capital. The previous year, she had inherited a sizeable amount of money from her late father, and knowing little about the finance world, had entrusted it to the ‘professionals’ at a top four banks’ investment arm. Her latest holdings statement showed that she had lost 40% of her father’s lifetime’s work in less than eight months. At a subsequent meeting with her investment managers, I asked the simple question, “Why did you have so much of her money employed at this stage of the cycle, at these valuations in such correlated assets?”

“We are not paid to manage cash,” they replied.

“You shouldn’t be paid to lose 40% either, in my opinion,” was the only response I could think of.

Of course, not many people, if any, will make money in a vicious, global equity collapse, but the person who loses least will be in the best position in the aftermath. But all over the world, investors knowingly or not are employing far too much of their cash at this stage of economic excesses and their non-risk holdings are far too small. People expect their money to be ‘working’ and fully committed and diversified, but not to be at risk. Unfortunately, it doesn’t work that way.

In the crash of 2008, every global equity market suffered severe losses. Blue-chip UK equity funds, emerging market funds, high yield and corporate bond funds all fell to varying large degrees. Property markets in many countries tanked, businesses failed, and unemployment soared. Very few asset classes went up. Some government bonds went up and mitigated some of the steep losses elsewhere, but people who thought that having a diversified equity portfolio covering many different countries were heavily disappointed as correlations went to 1 (i.e. all things move in the same direction).

It is 2018 and valuations are very high again, if not higher than the 2007 and 2000 peaks by many metrics. There are several warning signs of a new crash coming, but the party goes on for now, maybe for a while longer, but the investment climate is not good. Timing is everything and this is one of the cyclical worst times to be investing in most asset classes.

Our HindeSight Letter portfolio holds some ‘cheap’ stocks that at current prices have value. However, it is small in number as we are holding a large amount in cash. We believe strongly that this is the correct strategy at this juncture, as the risk/reward is just too skewed to risk. We urge investors to look into their portfolios held with their advisors and understand where they stand if there is another downtrade like 2008. Hopefully, not everyone will lose 40% again.

One of the assets that may well be uncorrelated, or even inversely correlated, in the next equity collapse is gold. The next section comes from a Hinde Gold Fund publication recently.

GOLD, July 2018

There are a thousand di!erent ways to analyse markets, including gold, and over the years we have done just that. But, nowadays, we tend to keep things as simple as possible. There is no perfect time to buy or sell any asset that works 100% of the time, but if you abide by a few hard and fast rules, you can considerably improve your investment timing and returns.

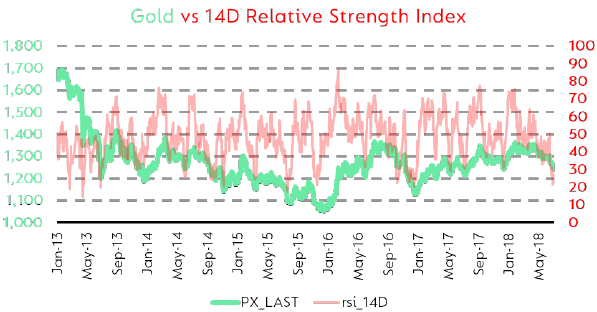

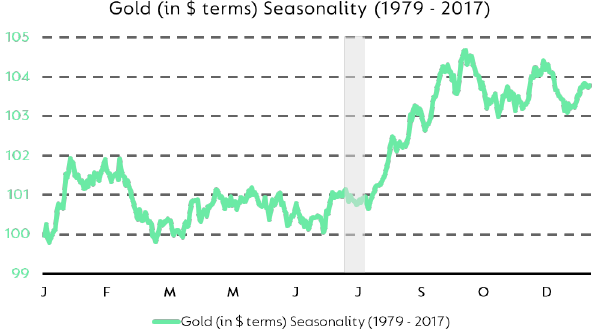

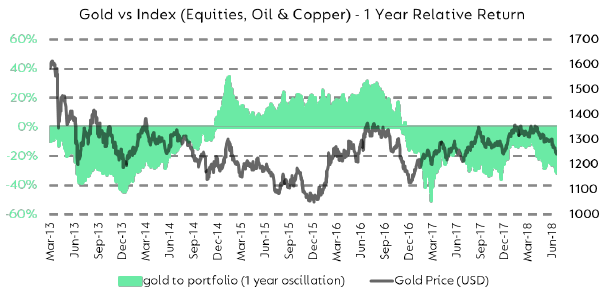

The four charts below show gold:

• From a technical perspective (relative strength indicator)

• From a seasonality perspective (differing returns for the time of year)

• Relative to other assets (an index of SP500 equities, Copper and Oil)

• Positional (how speculators are currently positioned)

The state of play for July 2018 is very clear.

• Gold’s RSI is sub 30, clearly very oversold

• It is July, a period when gold is strongly supported by second-half seasonal buying

• Versus the index of SP500, Copper and Oil, it is almost 30% cheaper on a rolling one-year oscillation

• Net speculator positions are under 10%, often associated with a low point in the gold price

All things considered, one should understand that this is an excellent time to add exposure to gold in your portfolio. This is not just for portfolio insurance, but also for the possibility of reasonable gains. There are many di!erent ways to access the gold market – gold funds, Gold Exchange Traded securities or just buying physical coins. But a platform called Glint is new to the market and it is revolutionising the gold market, allowing people to not only invest in physical gold and monitor it on a sleek digital app, but also to spend it via a Glint card.

WHY CHOOSE US?

HindeSight Letters is a unique blend of financial market professionals – investment managers, analysts and a financial editorial team of notable pedigree giving you insights that never usually make it off the trading floor.

We help our paid subscribers have 100% control to build their own portfolios with knowledge that lasts a lifetime and all for the price of a good coffee a month - just £4.99 or save 2 months by subscribing to our yearly plan, only £49.99.

Our history is there for all to see, measure and research.

Visit hindesightletters.com for more information