HindeSight Letters #87 April 2022 Newsletter - FREE TO READ ARCHIVED EDITION

HindeSight Letters #87 April 2022 Newsletter - FREE TO READ ARCHIVED EDITION

This archived edition of the HindeSight letter is completely free for everyone to read.

This is a taster of what you can get every month as a paid subscriber.

WHY SUBSCRIBE TO THE HINDESIGHT LETTER?

INVESTMENT INSIGHTS

Not only do we break down the reasoning behind our monthly share choices, we explain the methodology behind investing so you will learn more about strategies and how they impact your portfolio. Investing is like anything else, the more you know, the better you'll be at it and the better your decision to invest will be.

EMAIL ALERTS

You will also receive timely email alerts detailing portfolio changes to the HindeSight Dividend Portfolio #1, that covers FTSE350 stock as suggested by our Hinde Dividend Matrix and seasoned money managers. These are for immediate changes in opening or closing a position.

HINDESIGHT PORTFOLIO SELECTION

In our monthly HindeSight portfolio selection article we cover in-depth and in plain English, our reasons why we added the previous share to our portfolio with additional insights and performance data that's usually reserved for the trading floor.

OVERVIEW

Our overview features analysis, research & opinion on the latest news and current affairs and is a window into understanding factors that shape markets.

WHY CHOOSE US?

HindeSight Letters is a unique blend of financial market professionals – investment managers, analysts and a financial editorial team of notable pedigree giving you insights that never usually make it off the trading floor.

We help our paid subscribers have 100% control to build their own portfolios with knowledge that lasts a lifetime and all for the price of a good coffee a month - just £4.99. Our history is there for all to see, measure and research.

CONTENTS

OVERVIEW

HINDESIGHT PORTFOLIO SELECTION

INVESTMENT INSIGHTS

OVERVIEW

Apologies for the late arrival of the HindeSight Letter this month, I would like to say tiredness is my best excuse, but since I have been knackered since I was 12, it’s not a great one. Maybe, I have spent too long reading the news, wondering how on earth we have got here, rather like the car stuck in the tree. The observations of insanity seem endless at our current timeline juncture. I am sure history will judge us, (collective) accordingly.

In no particular order, the US-led geopolitical strategy with Russia, seems a good place to start, as we print ever more money to arm Ukraine to ‘bleed’ out a regime change, seemingly oblivious to the fact, that behind Putin, are even worse hardliners, often referred to as the ‘Siloviki’. Be very careful what you wish for. https://en.wikipedia.org/wiki/Silovik

Not to mention, the sanctions that are creating hardship, hunger, and cost of living crisis, which will continue to be seem in growing civil and social unrest across nations, with all the consequences of that. Next month’s topic, maybe. (note to self, keep adding tinned food to the weekly shop)

Playing poker with a nation, that has the largest nuclear arsenal in the world, for obvious reasons, doesn’t seem the smartest move. I have always liked the quote, that every Soviet school child knows. Made by Vladimir Ilyich Ulyanov, better known by his nom-de-guerre, Lenin, the ‘father’ of communist Russia, “Мы пойдём другим путём” (We will go by a different way), after the execution of his brother, for a terrorist plot against the Tsar.

With reference to Lenin’s quote, I certainly think we should have gone/go, (maybe too late) by a different way. I saw this passage written recently and couldn’t agree more.

It cannot be said too strongly: The US government must not be guided by any notion that a quagmire in Ukraine would drain Russian resources, diminish Russian influence and power globally, and possibly lead to regime change. The United States instead should do all within its power to help bring the war to a close rapidly in order to limit suffering; to eliminate risks that the conflict will widen and escalate, possibly to nuclear war; and to limit the negative global economic and food security repercussions.

A broader reason for determined efforts to end the war is the need to work toward restoring a relationship with Russia enabling cooperation on nuclear arms control and disarmament, climate protection, public health, and other vital matters of global concern.

US energy in helping bring the war to a close is also appropriate in view of the political responsibility of the United States, together with NATO, since the late 1990s in helping to create the conditions for a crisis. Actions having this effect included precipitously withdrawing from the Anti-Ballistic Missile Treaty in 2003, subsequently establishing missile defense facilities in Romania and Poland, and opening the door to Ukraine's membership in NATO in 2008.

In a recent paper, End the War, Stop the War Crimes, Lawyers Committee on Nuclear Policy outlines already widely discussed elements of an approach to ending the war. In brief, Russia and Ukraine should quickly agree to a cease-fire to enable negotiation of a settlement. Negotiations should then aim to end the war immediately and to resolve the overarching disputes concerning governance of the Donbas region and the status of Crimea. A longterm consultative mechanism could be put in place to resolve time-intensive or recurring issues and to help maintain peace and human security. Ukraine appears ready to forswear any possibility of joining NATO, so long as some form of guaranteed neutrality can be established, but seeks to join the European Union. The overall aim should be the preservation of Ukraine's sovereignty and territorial integrity in accordance with the UN Charter.

Source-Zerohedge.

And in the world of finance insanity, the esteemed Federal Reserve in the US, who just six months ago, ‘assured’ us that the inflation was ‘transitory’, (no laughing at the back), are having a F*** me moment, as not only is it blowing the doors off, but we now have 10 interest rate rises priced in for 2022. How did that happen? Could it have anything to do with that insane monetary printing and balance sheet expansion experiment we ran for the last 20 years?

But, that’s nothing compared to the Bank of Japan’s, (AKA-King Canute) continued policy, where they monetise their debt by issuing Japanese Government paper at the supported 0.25%, (Yield Curve Control, (ho-ho-ho) to ‘themselves’, while watching the interest rate differentials to the rest of word, skyrocket. And surprise, surprise, your currency goes into freefall. Guess what happens next, economics 101, as a country running a trade deficit, you import huge inflation, as the cost of imports in Yen terms moon shots too. You couldn’t make this up! Japan’s long term fight with core deflation looks set to reverse very shortly.

What do the Japanese import most, of course, it’s oil, which was on its own lunar trajectory in USD terms, but far worse in YEN terms.

Everywhere you look, insanity is in clear view. On a personal level, I am spending countless hours, fighting with a major UK insurance company, over a whopping £2,000 claim against a delivery driver, who crashed and destroyed my concrete gate post. Despite clear CCTV and witness testimony, (one minute you see it, next you don’t), the insurers are trying to defend their liability with preexisting damage claim. Now, I know that insurers have had a hard time generating investment income from upfront yearly payments with zero interest rates, but, the new depths of anything to wriggle out of paying, is reminiscent of the great Woody Allen sketch, “Deny, deny, deny”.

In the woke social media world, Elon Musk’s intended acquisition of Twitter has revealed much suspected behaviour, where the free-speech suppression algos have been lifted, benefitting many ‘out-of-favour’ figures, including ex-President Trump, with thousands of new followers. Bring back Goebbels, all is forgiven!

Last, and certainly least. The UK politicians seem hell-bent on internecine behaviour, whether it’s Tory MPs watching porn in the House of Commons or Labour MPs acting out the ‘Basic Instinct’ film scenes to distract their opposition colleagues, I am acutely aware, there was much better behaviour at a birthday party for eight year olds, that I recently attended.

As the legendary, Hyman Minsky often quoted, “Stability brings instability”. Well if you hadn’t noticed the ‘stability’ provided by cheap money, globalisation and much blind optimism is over. That time has been and gone, my friend.

The world is as unstable, geo-politically, financially or woke culture as never before, and it’s going to get worse, much worse.

HINDESIGHT PORTFOLIO SELECTION

SHARE OF THE MONTH APRIL 2022

ROYAL MAIL GROUP PLC - LSE:RMG

Portfolio ADD, 20/04/2022, 338p

RMG has appeared twice in the HindeSight Portfolio over the last eight years, Feb 2nd 2015, ADD price 428p (HSL February 2015) and 9th March 2017, ADD price 401p, (HSL March 2017) subsequently both recording 18% gains before CLOSE alerts.

As you can imagine, I am often asked what I think of XYZ company, and the prospects for an investment. In the case of ADD selections for the HindeSight Portfolio, for large capitalised companies greater than £1bn in value, typically, I respond with, “depends on the current price”, which is usually misunderstood.

With that in mind, RMG is a perfect example. I would not be a long-term holder of RMG, it is unlikely to demonstrate long-term earnings growth. It delivers mail and parcels. The commitment to dividend distribution from earnings did see shareholders receive over 10% yields over the last 12 months, but the price has dropped 40% since that time.

In HSL June 2021, in the Insights section, I briefly mentioned RMG, as one of those companies that spend their time, at the bottom of the FTSE 100, or top of the FTSE 250, due to the changing market capitalisation, like Birmingham City, a yo-yo type football club. As of the March FTSE 100 review, RMG stayed in the top flight by a whisker, really only because Evraz and Polymetal were demoted, as a result of their Russian operations. Currently, RMG, sits in 115th place, (see HSL June 2021 for review rules), by size, and will not be so lucky next time, if nothing changes.

http://www.hindecapital.com/attachments/reports/full/453/ original/UK_Newsletter_June-2021__3.pdf

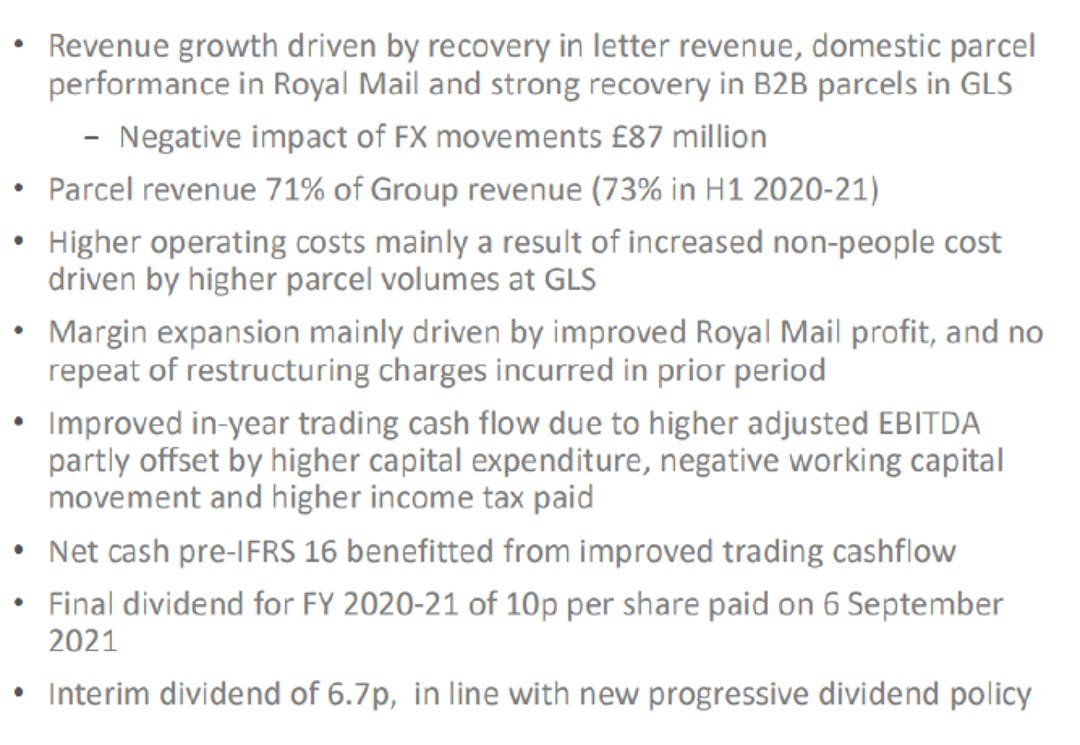

H1 2021-22 Group Financial Summary

Source: Royal Mail Group Analyst presentation

Returning £400 million to shareholders equally split between a share buyback and a special dividend.

Source: Hargreaves Lansdown

While I did see that RMG put up the price of 1st class stamps to 95p from 4th April, as you can see from the above financial summary, RMG’s revenue comes mostly from parcel deliveries, where it holds almost a third of the UK market share, naturally, with Amazon breathing down on it.

But, ultimately, the ADD notification, merely reflects that it is currently undervalued, and far more likely to see a mean reversion to fair value over the next nine months than further price erosion. It has the usual bad news about ‘pay discussions’ with its unions, but they may well be fully priced in at these levels. Earnings growth shouldn’t be discounted either, but with forward P/E ratios hovering around only 5X, the cheapness is there already.

Let’s see if RMG does better than Birmingham City over the next few months.

INVESTMENT INSIGHTS

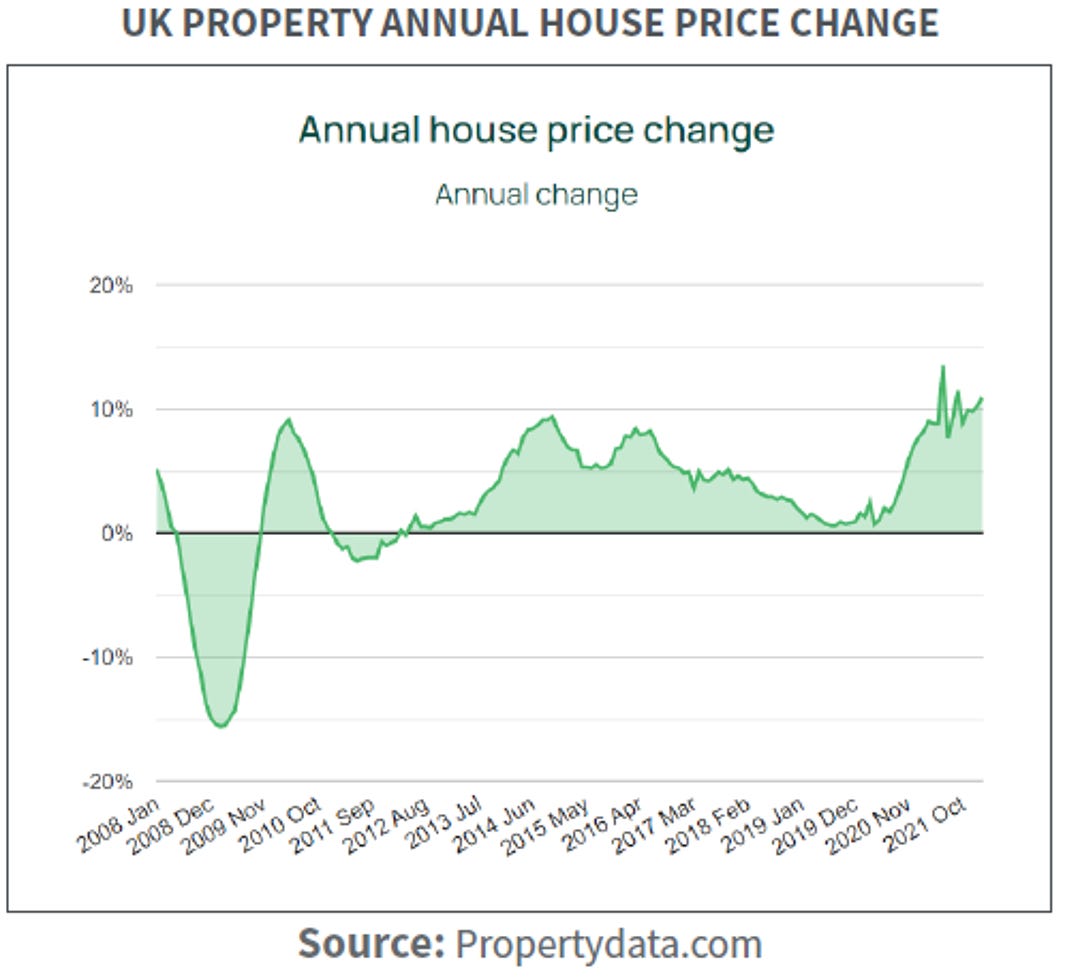

It is an unwelcome call to suggest that “Peak Wealth” has been experienced, certainly in the UK, where we are far too focused on the value of our houses, which have certainly seen strong growth in many areas and postpandemic recoveries in others.

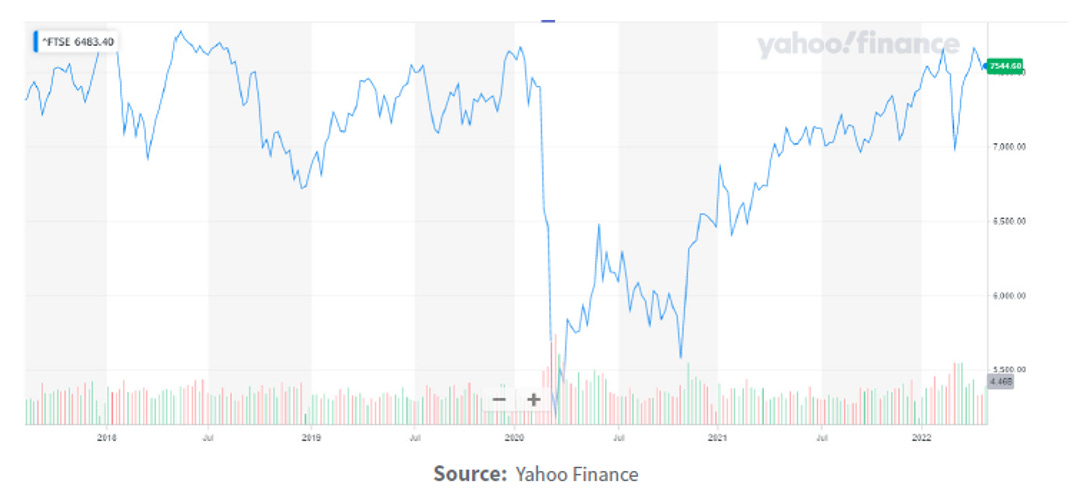

But, with the FTSE 100 broadly at the same level it was five years ago, including a pandemic 30% slump and a less dramatic 10% Ukraine invasion, the passive index holder is having to get by on 3.5% dividend yields for wealth creation in UK equities, with money printing support waning.

I know many readers are happy to stick to the “Permanent/ Cockroach portfolio” of Equities, Bonds, Gold and Cash, which historically has given growth and substantial protection. But, even that strategy looks challenging for the foreseeable future with bond prices continuing to fall, gold languishing and cash holdings being inflated away at an alarming rate.

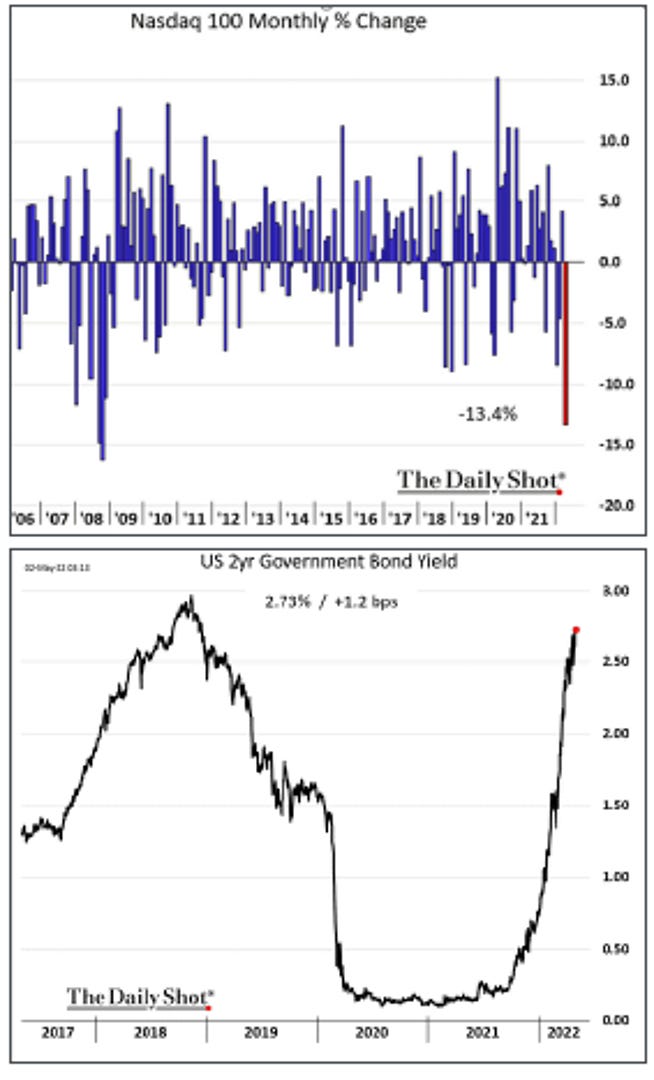

It could be worse and it has certainly been an unpleasant time for some of the legendary US market outperformers, that went by the “FAANGS” acronym, Facebook, Apple, Amazon, Netflix and Google.

There is an old saying in the financial markets regarding price chart patterns, “Up by the stairs, down by the elevator”, which has unfortunately been experienced by Netflix in recent weeks. It has been generally observed that the “FAANGS” have held the general market indices up over the last few years, so with the new “FAAGS”, we shall have to see whether they can manage to do the same now.

I just read that legendary macro trader, Paul Tudor Jones, commenting that the current valuations and climate are the worst conditions ever for invested capital in stock and bond markets, but as always there is often a period of time when Road-Runner is in mid-air, unaware of the drop below. Conditions that have been internally deteriorating for years, have been plugged by the central banks money machine but with roaring inflation, even they can’t continue.

Let’s completely forget about fixed income for now as that is a lost cause, but for equity portfolios, the passive index investor will have to understand that the old text book lessons, may come in handy, and select a basket of stocks that are large, undervalued, pay reasonable dividends and haven’t got years of unrealised earnings growth already baked in the price.

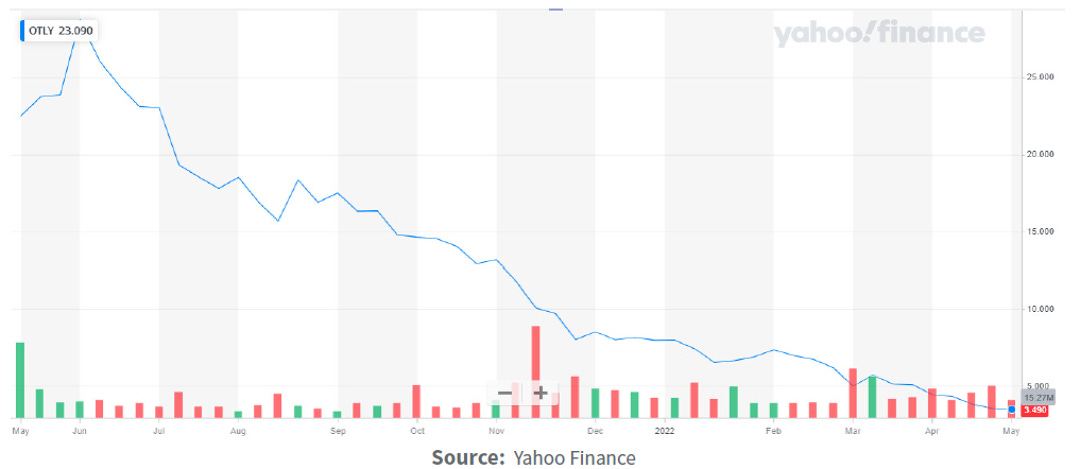

Take Oatly Group, (Dairy alternative food group), once darling IPO, just a year or so ago, now down 90% in the latter group. There are more of these bad stories than there should be.

Relative to BHP, large mining conglomerate, paying substantial dividends in the former group.

HSL ADD 27/08/2021 HSL CLOSE 01/04/2022 (217 days Holding) Total returns 48%, including 8% dividend payments.

Almost a decade ago, when we first started writing the Hindesight Dividend Letter, it was the belief that all investors, big and small, could benefit from understanding that there were merits involved in not blindly investing in equity indices, or with fund managers who hug the index, “passive investing”. Stock selection, of large, well capitalised companies, paying good dividends at low valuations in their stock cycle with rotation, is not just one of the best risk-adjusted methods for compound return, but an excellent defence in bad times as well. And that might come in handy rather than relying on continual annual % growth in house prices in the UK at such huge multiple of income amid rising interest rates.

Visit hindesightletters.com for more information