HindeSight Letters #84 January 2022 Newsletter - FREE TO READ ARCHIVED EDITION

This archived edition of the HindeSight letter is completely free for everyone to read.

This is a taster of what you can get every month as a paid subscriber.

WHY SUBSCRIBE TO THE HINDESIGHT LETTER?

INVESTMENT INSIGHTS

Not only do we break down the reasoning behind our monthly share choices, we explain the methodology behind investing so you will learn more about strategies and how they impact your portfolio. Investing is like anything else, the more you know, the better you'll be at it and the better your decision to invest will be.

EMAIL ALERTS

You will also receive timely email alerts detailing portfolio changes to the HindeSight Dividend Portfolio #1, that covers FTSE350 stock as suggested by our Hinde Dividend Matrix and seasoned money managers. These are for immediate changes in opening or closing a position.

HINDESIGHT PORTFOLIO SELECTION

In our monthly HindeSight portfolio selection article we cover in-depth and in plain English, our reasons why we added the previous share to our portfolio with additional insights and performance data that's usually reserved for the trading floor.

OVERVIEW

Our overview features analysis, research & opinion on the latest news and current affairs and is a window into understanding factors that shape markets.

WHY CHOOSE US?

HindeSight Letters is a unique blend of financial market professionals – investment managers, analysts and a financial editorial team of notable pedigree giving you insights that never usually make it off the trading floor.

We help our paid subscribers have 100% control to build their own portfolios with knowledge that lasts a lifetime and all for the price of a good coffee a month - just £4.99 or save 2 months by subscribing to our yearly plan, only £49.99.

Our history is there for all to see, measure and research.

CONTENTS

OVERVIEW

INVESTMENT INSIGHTS

OVERVIEW

In October 1962, in response to the deployment of American ballistic missiles in Italy and Turkey and in the aftermath of the failed Bay of Pigs invasion by CIA-trained Cuban exiles, the USSR and Cuba agreed to establish Soviet missile bases on Cuba. In the month that followed, the world, arguably, came as close to WWIII in the whole half century of the Cold War. With Cuba, only 90 miles in distance from the southern tip of the US, making up for some beliefs of Soviet missile inaccuracy, the threat of Mutually Assured Destruction became very real.

Fortunately, the diplomatic outcome led by US President John F. Kennedy, sadly, in the last year of his life, resulted in an agreement to remove all the missiles from these countries, although the Italian and Turkish withdrawal was not publicised at the time.

The North American Treaty Organisation, (NATO), was created on 4th April 1949. (An advancement on the Treaty of Dunkirk in 1947, which was signed by France and Great Britain as a Treaty of Alliance and Mutual Assistance, in the event of attack by Germany or the Soviet Union after WWII). The 12 original founding countries were, US, UK, France, Italy, Iceland, Portugal, Canada, Luxembourg, Norway, Netherlands, Belgium and Denmark with Greece and Turkey joining in 1952 and lastly (West) Germany in 1955. Apart from the post Franco-era addition of Spain in 1982, the NATO membership remained unchanged until the late 1990’s. NATO’s primary mandate is one of collective security, whereby its independent member states agree to mutual defence in response to an attack by any external party.

In the period following the collapse of the Berlin Wall in 1989 and post the 1991 decline of the communist Union of Soviet Socialist Republics, the ‘thirst’ for ‘democracy’ has seen the expansion of NATO eastwards, gobbling up the pre- Russian satellite countries. Firstly, Poland, Czech Republic and Hungary in 1999, followed by Bulgaria, Estonia, Latvia, Lithuania, Romania, Slovakia and Slovenia in 2004, with the last of ex-Yugoslav countries since. Many of the remaining old Soviet States, including Ukraine, have now become NATO partner countries, further adding to the compression of the Russian bear.

You can clearly hear Putin’s voice bellowing, “Stop f****** pushing”.

Well, there are Russian warships heading through the English Channel on route to the Crimea and 100,000 Russian troops with Kyiv in their sights, and still no one is listening. Ooh, sanctions…ffs.

Prior to WWII, British Prime Minister Neville Chamberlain used the phrase, “A small country, far away, about which we know little” with reference to Czechoslovakia, which has become infamous for the betrayal of a small country by a large power and the appeasement of an aggressor. Ukraine, hopefully, will not suffer the same fate. But, many do not understand that while a sovereign country, Ukraine, does not enjoy the national unity that that would suggest. Its history and culture demonstrate the divide of a border state, its very name, meaning just that in old Slav. Throughout time, West and East Ukraine have often fought on opposing sides with the larger powers, and the East today, still has more Russian attachment, including language than the western half. But, our media in the West, (on a good day) is as biased as the media in Moscow. Who is threatening who? Is it the West’s continual pushing missiles and armaments eastwards or Russia threatening to push back. Objectively speaking, both sides are clearly at fault, but, history has told us, that this is how wars start.

Geo-politics is a dirty game, everyone has their own agenda.

The US continues to try and maintain its global military superiority. It has the ability to provide financial ‘support’ and ‘security’, while the finances inevitably find its way back to the US arms contractors, as Eisenhower always warned us. Enlarging NATO eastwards, continues to be well supported by the powers that be, placing advanced missilery on those soils. But, is the current crisis not just another powder keg, like 1962.

Russia has the biggest mining industry in the world, with vital reserves of oil and gas. The once superpower still has the most nuclear weapons and one of the largest standing armies. Under Putin’s long leadership, it wants to be respected and feels constantly threatened by the West.

Germany, as in the Cold War, sits in the unenviable position of middle Europe, knowing full well, that any conflict that gets out of hand will no doubt see their homeland in the warzone. It has to play a strange hand of cards, knowing that since the demise of its nuclear energy industry, (blame the Greens/Climate change brigade) it is increasingly dependent on energy, some 40%+ from Russia, with the allure/bribe of the Nord Stream2 pipeline. Small diplomatic conciliatory actions such as refusing UK deliveries of arms bound for the Ukraine to travel through their air space seem a tricky play for the NATO country.

While China knows its desire for status and industrialisation for its huge population can’t come from within. It has to buy world influence and import vast quantities. It has 20% of the world’s population but only has access to 7% of the water, requiring some nifty ‘restructuring’ of waterways that are already creating problems throughout the Indian sub-continent. As the largest producer and consumer of coal, providing 70-80% of the energy needs, any climate change actions by other countries, are clearly, a proverbial p*** in the ocean. Their financial clout is being matched with their military advances and potential territorial ambitions, while snubbing out democracy in Hong Kong in less than a year, 26 years ahead of the 1997 agreement. Sadly, as a long-term visitor, Barbados has now sold out to the Chinese as well. No doubt, some debt-relief promises were all it needed to force through a hasty decision to remove the Queen as their head of state. A very sad state of affairs, but closer at home, we now understand that Chinese spies and influence are wielded in the UK parliament.

The UK, that once was the most influential country across the globe, only has concerns on whether there was a party or not in Downing Street. I wouldn’t be surprised if the average UK media uneducated woke reader is completely oblivious to the tinderbox we have awaiting, as each dawn goes by.

I read recently that the legendary investor Jeremy Grantham once remarked the stock market is like a Brontosaurus. Its nerve system is so primitive, that it takes a week to notice it has been bitten on the tail. But, it seems to be feeding through slowly.

With the highest equity valuations in recorded history and the highest bond prices, in 2021, it is not an ideal situation with any margin of safety to have 7% and rising inflation with WWIII looking like it’s going to kick off any time.

For now, we seem to be back to Captain Mainwaring’s dilemma, with Corporal Jones’ infamous phrase, “Don’t panic” facing Private Fraser’s “We’re doomed” outlook.

Visit hindesightletters.com for more information

INVESTMENT INSIGHTS

A month ago, I wrote, “Fearful is the word that most springs to mind as we enter 2022”. Unfortunately, it seems to be becoming widespread far too fast. WW3 concerns and 7%+ inflation haven’t helped. Throughout 2021, it was well documented in the financial press, that I read, that equity and bond valuations were far in excess of historical levels, while inflation was starting to rise by increasing degrees. In the main, these situations have been created by the insane monetary policy employed by the global central bankers, pinning interest rates at zero, while continuing to add trillions of dollars more into the system by asset purchases. The urge to speculate, when the risk-free return is zero, is vastly enhanced, and the ability to extrapolate huge growth multiples on equities, (especially new IPOs), follows suit, until challenged. Think roadrunner over the cliff.

The current HindeSight Portfolio, as one might expect, amid these valuations, is contained and defensively, but very cognisant of the declining purchasing value of cash. But, we still closed out four holdings, Royal Dutch Shell, (+63%), Sainsburys, (+38%), Tesco, (+35%) and GlaxoSmithKline, (+38%) and have not added any stock or research to our holdings this month, although Unilever was a potential choice.

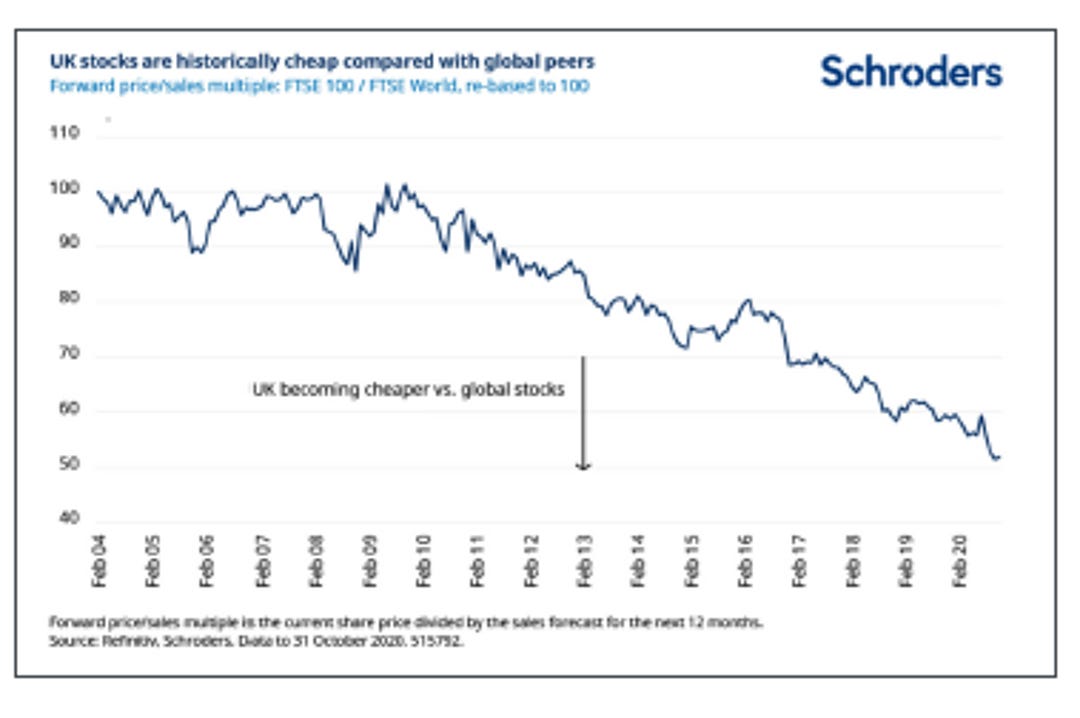

While the US equity indices, are held up by the five main stocks for now, and the UK’s relative ‘cheapness’ has been supportive in January, some portfolios may already be looking decidedly less rosy a month into the new year, than in 2021. It hasn’t made any sense to me, for a long while, to own fixed income assets, with far lower yields than inflation, guaranteeing an inflation-adjusted real loss, but as the bond market is the largest asset class in the world, it makes up most of many portfolios.

In the second week of January, we saw the largest % loss since 1973, in US 30-Year Bonds. I always like reading John Authers’ Bloomberg comments, recently he recounted the old Irish joke, when asking directions. “If I were you, I wouldn’t start from here”. I’m sure every central banker is only too aware of that conundrum today. Sky high valuations and roaring inflation, while you are starting to talk about withdrawing liquidity and raising interest rates from zero. Are those deer I see in the headlights?

But, there are many other ways, your portfolio could be heading south.

A quick glance at some of the high flyers in 2021 tells a sorry story.

The UK IPOs’ returns should remind us again, that hype and hope, with huge growth optimism built into the price have never been the best of strategies at the top of speculative cycles. While the great two-way trading vehicles of Cryptos do not offer sensible long-term value investment holdings.

It’s no surprise, (to me, at least) to see a few of my pet hates fall from totally unjustifiable valuations and look particularly sick, e.g. Trust Pilot, Wise and Trainline, but there are many others that were equally vulnerable.

Having observed first hand, the stock market crashes since 1985, the vicious 10% sell-off from the December highs in the US indices is certainly the way it starts, but bearing in mind, we are only back to September’s prices, it’s easy and indeed possible, to dismiss this correction from Xmas excess. And the UK market seems very well supported. The trouble for the dip buyers and passive investors, to my mind, is far too much, (nearly all) of the potential future input data/scenario analysis falls on the negative side of the coin, with very little priced in.

• WWIII/A small incursion, (Biden allowable)/ diplomatic solution

• Energy prices continuing to rise/spike on above

• Inflation rising across the globe as negative real interest rates continue to push

• The IMF already adjusting growth rates down worldwide, as post-pandemic hopes are muted

• Central bankers unable to cut rates and add liquidity in any fashion like the last 30 years

• If it’s not Russia/Ukraine, there still remains a growing China geo-politic risk, which is no longer the growth engine and deflation exporter of the last two decades

In many ways single stocks, like Wise, the FX transfer platform, down 50% since 2021 highs, may well represent the risk to the whole market in many asset classes. It is an excellent company, with great products, that offer real value and use to its client base. But, last year’s prices had far too much hope and future growth built in and the perceived ‘worth’ and opportunity cost is very different today. The move from hype/hope through reality to despair is unfortunately often large in % terms and can have very material relevance to many portfolios. Whether, this current January debacle continues has yet to play out, but for me to have more optimism, I really do need to see some, (any) positives on the above list, to be anything other than very defensive at this time, but lower entry price levels may be the best positive to hope for, in investment terms for most assets, apart from precious metals which should still be a firm addition for some portfolio protection.

Speaking of precious metals, some readers might be interested to join a free Zoom call being given by Simon Popple, of www.brookvillecapital.com on Thursday 3rd February at 7pm London time, where he will detail their methodology for returns in this space. He will also be introducing Chris Berlet, CEO of Stakeholder Gold, (TSX.V:SRC.V) and their operations which has been written about in the HindeSight Letter over the last year.

Join us on Zoom https://zoom.us/join

Meeting ID: 284 867 3504

Passcode: 202162

Visit hindesightletters.com for more information