HindeSight Letters #81 September 2021 Newsletter - FREE TO READ ARCHIVED EDITION

HindeSight Letters #81 September 2021 Newsletter - FREE TO READ ARCHIVED EDITION

This archived edition of the HindeSight letter is completely free for everyone to read.

This is a taster of what you can get every month as a paid subscriber.

WHY SUBSCRIBE TO THE HINDESIGHT LETTER?

INVESTMENT INSIGHTS

Not only do we break down the reasoning behind our monthly share choices, we explain the methodology behind investing so you will learn more about strategies and how they impact your portfolio. Investing is like anything else, the more you know, the better you'll be at it and the better your decision to invest will be.

EMAIL ALERTS

You will also receive timely email alerts detailing portfolio changes to the HindeSight Dividend Portfolio #1, that covers FTSE350 stock as suggested by our Hinde Dividend Matrix and seasoned money managers. These are for immediate changes in opening or closing a position.

HINDESIGHT PORTFOLIO SELECTION

In our monthly HindeSight portfolio selection article we cover in-depth and in plain English, our reasons why we added the previous share to our portfolio with additional insights and performance data that's usually reserved for the trading floor.

OVERVIEW

Our overview features analysis, research & opinion on the latest news and current affairs and is a window into understanding factors that shape markets.

WHY CHOOSE US?

HindeSight Letters is a unique blend of financial market professionals – investment managers, analysts and a financial editorial team of notable pedigree giving you insights that never usually make it off the trading floor.

We help our paid subscribers have 100% control to build their own portfolios with knowledge that lasts a lifetime and all for the price of a good coffee a month - just £4.99 or save 2 months by subscribing to our yearly plan, only £49.99.

Our history is there for all to see, measure and research.

CONTENTS

OVERVIEW

INVESTMENT INSIGHTS

HINDESIGHT PORTFOLIO SELECTION

OVERVIEW

Fortunately, my wife doesn’t give the monthly HindeSight letter more than the occasional, cursory glance, “Your letter guff”, as it is frequently referred to. In the almost two decades of our relationship, I can safely say that I have never received a birthday or Christmas present that I have ever hinted at, or greatly appreciated on receipt, until now! But, in July, I was given a brass, antique-looking, but fully functioning telescope with a magnification capability of a whopping 36X.

From my, more used-now, home office, where Spike Milligan once wrote far more exciting prose than the HindeSight Letter, I am blessed with a 180° vista of the English Channel, from Hastings in the West and Dungeness’s two nuclear power stations in the East. While the telescope has become a truly fascinating addition to my boat watching among other local interest!, the distant towers of the Dungeness have been brought dramatically into view.

In 1965, Dungeness A was one of the earliest nuclear power stations built, only ten years after the UK government published a white paper announcing the development of the purely commercial, nuclear program. The world’s first commercial nuclear reactor, Calder Hall 1 was completed at Windscale, (now Sellafield) , and opened on October 17th 1956, by Queen Elizabeth II. At the time, Anthony Eden’s Conservative government, remarked, “that Britain has become the first nation anywhere in the world to produce electricity from atomic energy on a full industrial scale”.

The Suez crisis that erupted less than a month later, lead to another a white paper, titled ‘Capital Investment in the coal, gas and electricity industries which proposed increasing the nuclear build program’, to maintain an ability for power self-sufficiency for its growing post-war population and industrial needs. At its peak in 1995, nuclear energy provided 26% of the electrical usage, with more than 20 reactors connected to the grid, but it has been in decline since. While Dungeness A was shut-down in 2006, Dungeness B, which was completed in the early 1980s continued, (the civil part of the construction was done by Balfour Beatty, where my father worked at the time and he remembers many site visits there).

During the Covid-19 pandemic, in 2020, two nuclear engineers, designated key workers from Northumberland, stayed in our holiday let for many months, their task to re-investigate the viability of reversing the 2018 decision to close Dungeness B. I discussed the subject with them at the time, (while social distancing) and remember one of their comments, “Someday we might just need this, if Russia plays silly buggers”. Unfortunately, I presume this was unsuccessful, with the recent decision, to continue the close down, and yet another power station has bitten the dust, leaving only eight in current operation today, still supplying 18-20% of UK electricity. Most of the existing stations are looking to shutdown and defuel, (a lengthy and costly process) within the next ten years. Only Hinkley C, has real potential to come on line in the near future, while the nuclear sector as a whole, now in private hands, looks to be floundering in the unknown. The possibility seems clear enough that in time, the 1950s ground breaking technology will have had its day, with wellknown nuclear disasters, geological waste concerns and importantly, unforeseen closing, terminal cost issues being behind its demise.

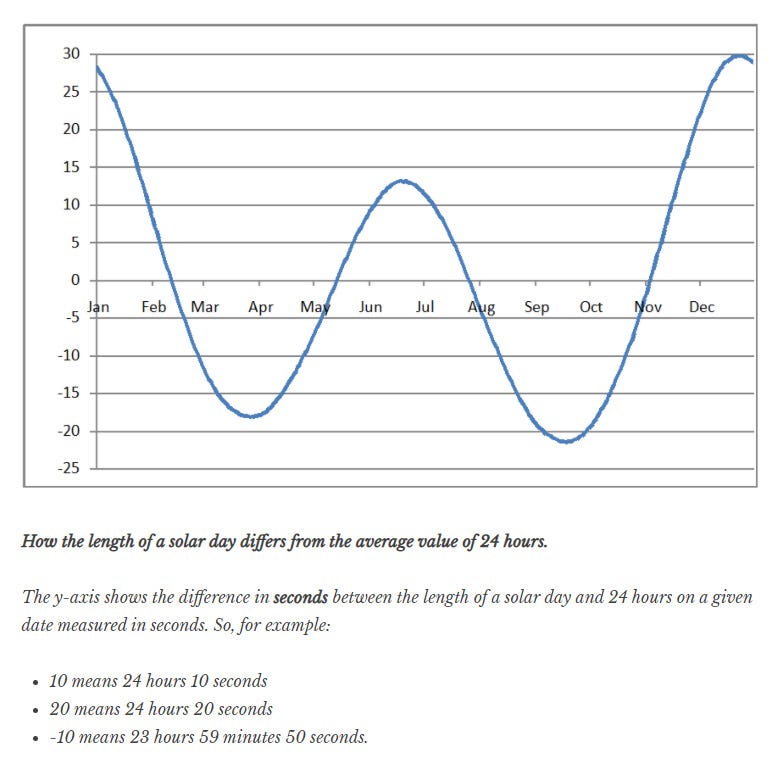

In southern England, the June summer solstice, comes with a day length of 16 hours and 38 minutes, but by the time of the December winter solstice, we are reduced to a mere 7 hours and 49 minutes, a drop of 8 hours and 49 minutes, a theoretical average daylight loss of 2.9 minutes a day. But, due to the 23.5°tilt and elliptical orbit of the Earth around the sun, the rate of day length is not constant. In fact, in late June-early July and in early December, the average day loss is roughly a minute, but in September and October, the day loss rises to over 3.5 minutes. Bung in the daylight savings adjustment in late October and the darkness becomes very apparent, quickly. Always a good time to discuss the current concerns of power cuts amid rising gas and electricity prices. Unfortunately, I am old enough to remember doing my homework by candlelight in the mid-70s, amid the coal miners’ strikes and the infamous 3-day week. But, could it really happen in 2021, in our age of technology and all the needs we have today for electricity?

What exactly has happened/is happening to get to this ridiculous state of affairs and will concern lead to full-on crisis just after we appear to emerging from the Covid-19 crisis, or will it blow over?

What part does ineptitude, complacency, 21st century bull market optimism/wishful thinking or good-old fashioned geo-politics play in these matters?

We seem to have been bombarded in the news recently across this spectrum of possibilities, but everything to me seems to stem from three main factors;

• The desperate urge to move away from fossil fuels in a record timeline

• The over-reliance on smooth trade and supply lines

• Piss poor planning

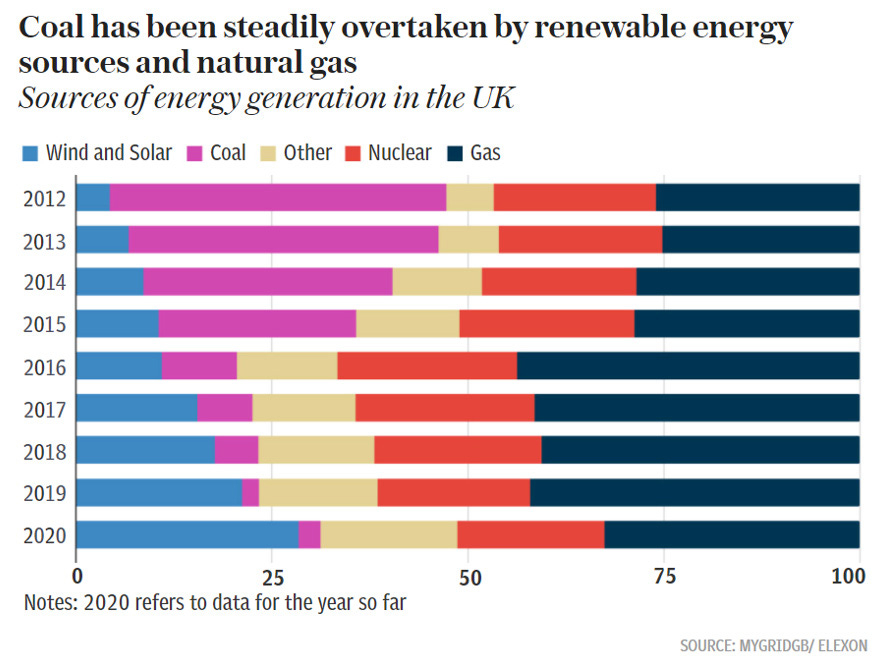

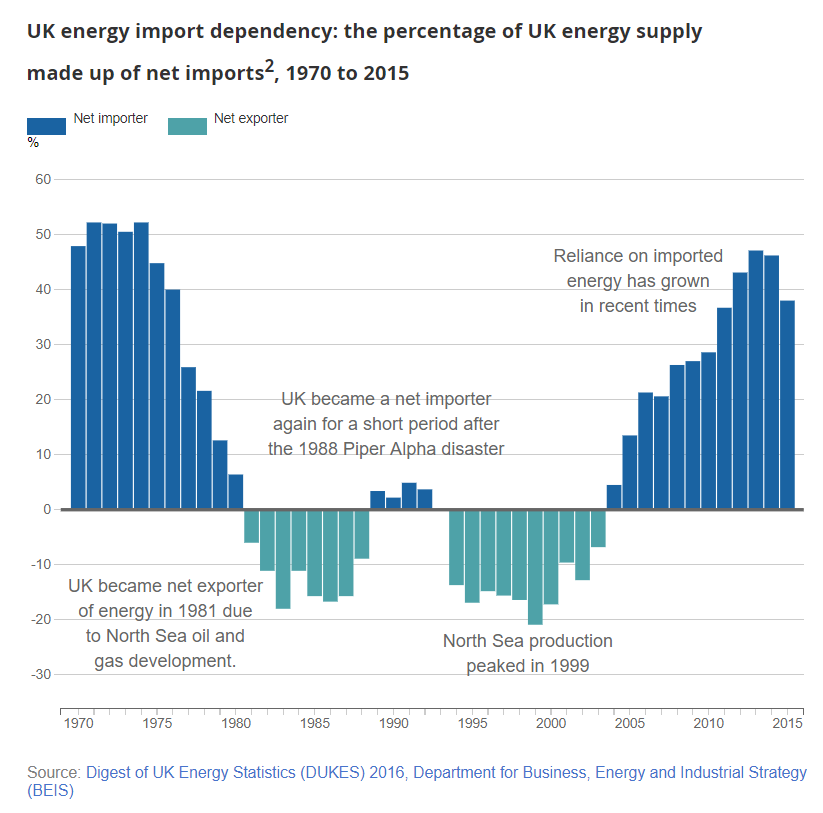

Only 15 years ago, the UK was a net exporter of energy with an abundance of North Sea oil & gas reserves, strong nuclear sector, still active coal production and great advances in the world of renewable energy. But, not now.

On 21 April 2017, the UK went a full day without using coal power for the first time since the Industrial Revolution. We are clearly doing an amazing job of replacing coal with renewables, (approaching 50% of demand), mainly wind and solar, abiding by most of the western nations commitment to combat the current climate change, if it is indeed, man-made. The drawbacks come with the difficult task of using that renewable energy, when it occurs, as storage is much more problematic and the variances in wind and solar output in any month. Not to mention, the fact that China doesn’t care. The phrase “drop in the ocean”, springs to mind.

In fact, due to lack of wind/wrong type of wind? on a warm early September day, EDF was asked by National Grid ESO, who balance the UK’s electrical supply, to fire up West Burton A coal station, that had been on standby to meet the deficit of just under 3%.

Any country that imports essential goods, like energy has to compete on the world’s trade markets for those goods, and typically, that comes with the dynamics of supply and demand, now and future planning, with price, usually the balancing factor until crisis point.

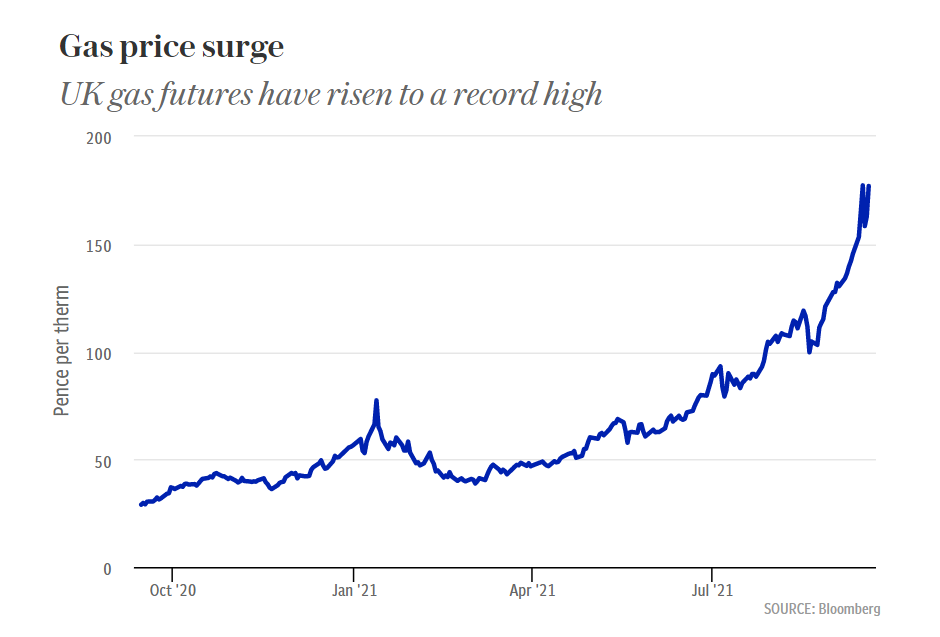

Only last year, the oil price in the US main hub, traded at negative prices due to over supply with no storage to be had at any rate as Covid-19 spread through the economic world. As the economies ‘emerge’ strongly, driven more by the insanity of central bank money printing than actual real growth, over-supply has been supplanted by huge demand across the globe. The price of natural gas, a significant input for electricity conversions has rocketed by 250% in 2021 and still heading higher. Of course, there is no long-term shortage of natural gas, whether it comes from Qatar, Russia or the US, but in the short term, ie NOW, it is a different story. From Evergreen, the pathetic ship stuck in the Suez Canal in March this year, US tropical storm season and Russia levering their exporter position to force through the Nord Stream 2 pipeline into western Europe, (held to ransom long-term-bad plan) supply constraints are apparent. We even have an issue with fire damage to the IFA1 interconnector, used to import electricity from France, just up the road in Ashford, reducing import ability for the next six months. Not ideal, bearing in mind the French hated us before Brexit, now we have gone and rubbed their noses in it with the recently announced AUKUS pact, between US, UK and Australia in the South Pacific.

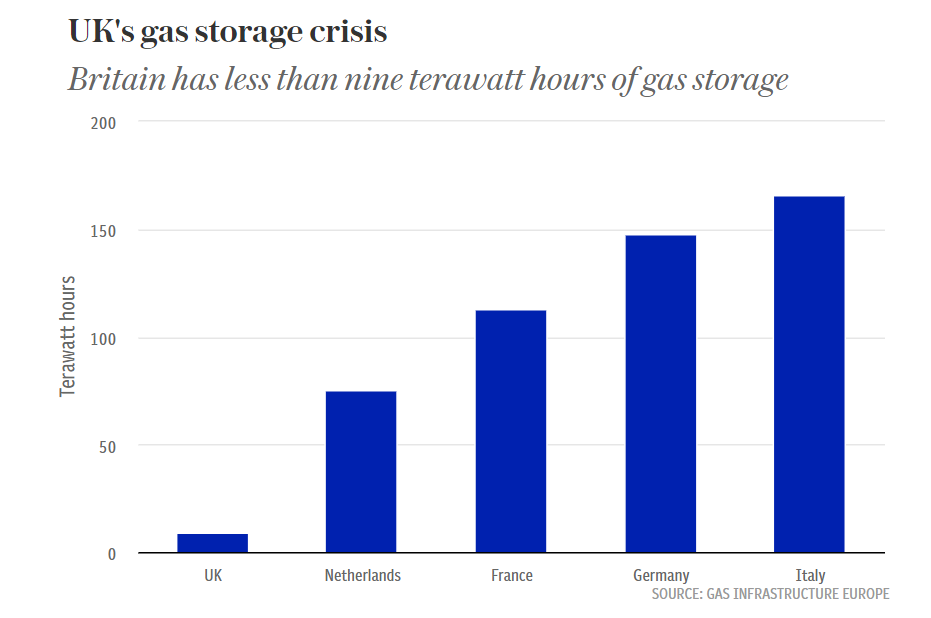

Even, the most basic of back up plans, think spare petrol can in garage, on a bigger scale, seems to have been overlooked as our gas supplies look woefully short in comparison to European countries. This slides nicely into the wishful thinking/piss poor planning section.

Looking for a couple of gallons of diesel, willing to swap for a doctor's appointment.

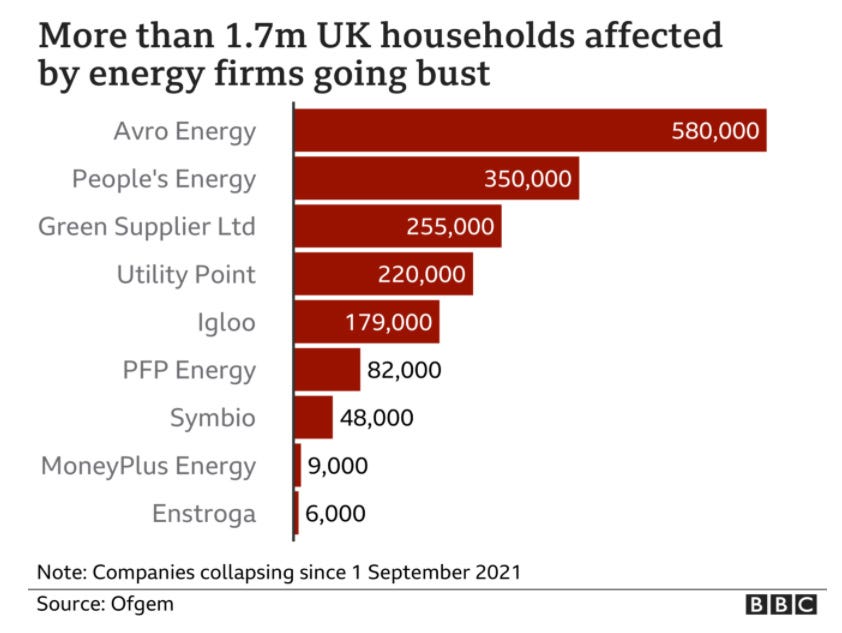

One thing is for sure, we will all be paying more for electricity in the next six months, significantly so. The 2014 Ofgem report that promoted competition in the energy sector away from the oligopoly of the ‘big six’ suppliers, over the last five years, appears to be blowing up as I write. There were 70 electricity suppliers at the start of 2021, with rumours that less than 20 will survive to see 2022. What is happening seems nothing more than the smaller suppliers got caught short providing ‘cheap’ electricity to their customers at the Ofgem cap level, new rate in August, (£1277 per unit, up 12%), while being contractually forced to pay many multiples of this in the open market. “Hedge”, what’s that then? (Incompetence/ Wishful thinking/Piss poor planning again). My current provider Symbio looks to have joined to luckless fray. Splendid. It looks like we are moving back to the main players to stay the course and pick up newly distributed customers, probably with a bit of government support. It might well turn out well for the cabal again, see HSL stock pick this month, LSE:SSE Plc.

It’s over a century since Foreign Secretary, Sir Edward Grey, quoted his infamous lines, “The lamps are going out all over Europe, we shall not see them lit again in our life-time”. Well, I don’t think it’s that bad but it wouldn’t be the worse spend for £150 to buy back up charger packs for your laptop and phones, with an old style plug-straight into wall socket phone, as a back-up plan this winter, on the days when electricity might be hard to come by. Meanwhile, in other news, there is a HGV driver crisis, with the average driver age of 53, we are apparently 100,000 short. (Can either of those stats really be true!!)

INVESTMENT INSIGHTS

It feels that too many months of late, (ominous in itself) I have written in the Insights section, somewhat of a summary of the investment and trading opportunities that are ‘blatantly’ apparent, to me at least, in the current market. In my career, I have arguably done much more trading, which I would have to define as short-term, rather than investing, with a longer-term perspective. As a market-maker in US Treasuries for many years, trading might well be measured in hours or intra-day. The P&L could be easily defined if you started and ended the day with a flat position, and the day’s trading had created either a credit or debit balance by close of play. Market makers often move into proprietary trading with a more intra-week or intra-month mentality, but knowing your expertise with respect to horizon is crucial to maximising your return profile. Investing is a different game, whether with your own money or the bank/funds with the horizon in many cases, far more open-ended and less determined.

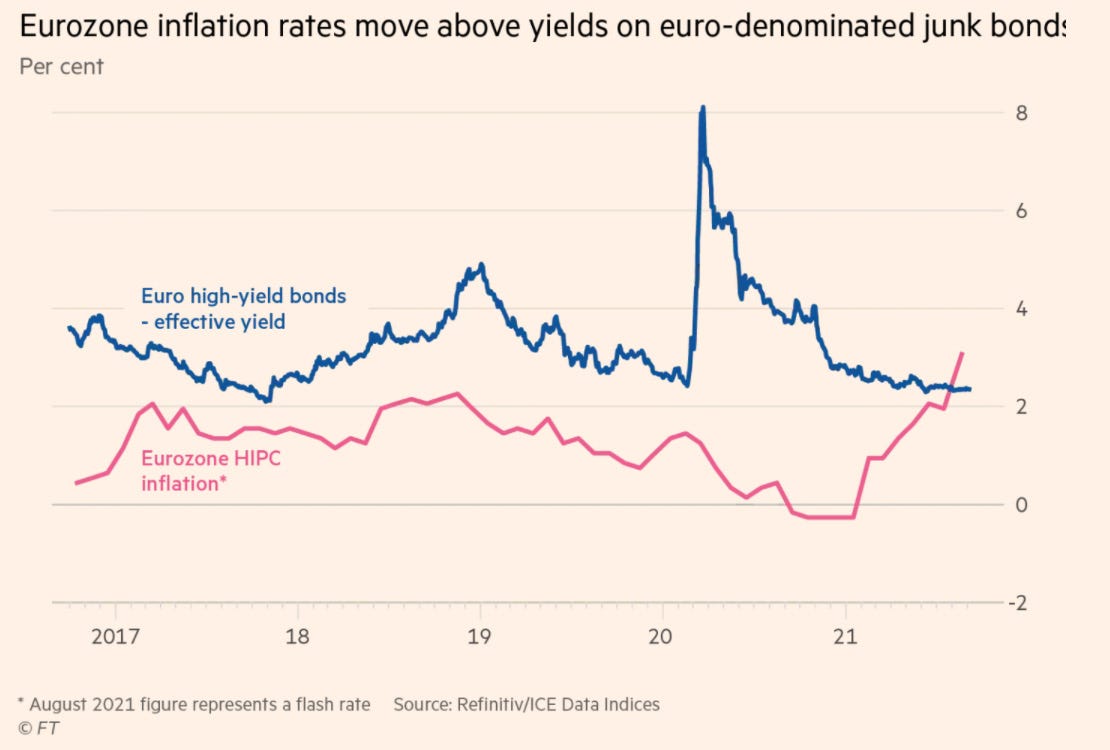

I often draw comments and graphs from John Hussman’s excellent monthly market letter, www.hussmanfunds.com . He started his September letter with the extract below, from Benjamin Graham which I feel is too good not to republish. Warren Buffet and Sir John Templeton were both students of Graham, but most value traders are struggling, no doubt, with the current investment opportunities.

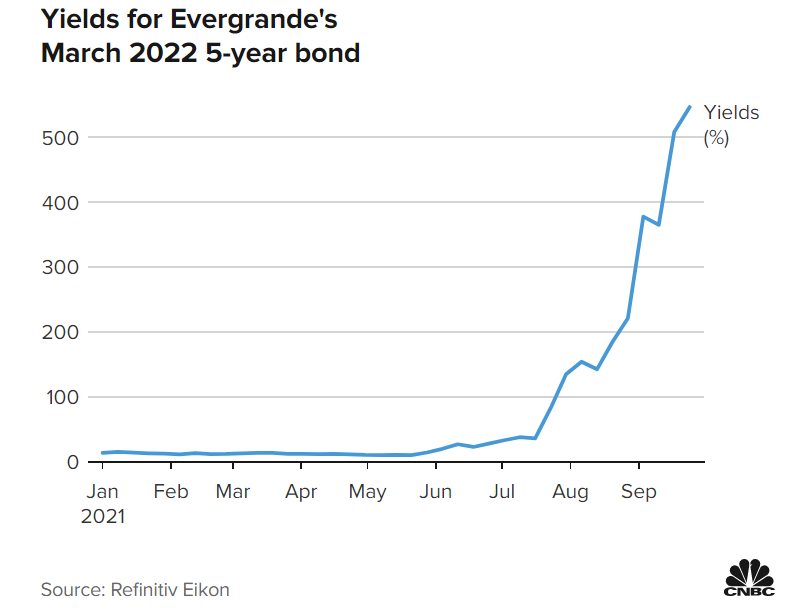

Graphs such as above, literally jump out at me. The splendid opportunity to buy junk bonds that on average guarantee you a loss after inflation for the first time ever! Sign me up. You only have to look at the recent debacle with China’s property giant, Evergrande with yields skyrocketing and subsequent bond price drops to understand Graham’s reference to “Safety of principal”. Not to mention, hot off the press, after a small, negative report in the FT, last week, Alphawave, the Canadian chip maker, a much publicised London IPO of 2021, dropped 50% in a day. At 170p on 29th September, it is a far cry, and 60% from the listing price. Hmmm.

'' An investment operation is one which, upon thorough analysis promises safety of principal and an adequate return. Operations not meeting these requirements are speculative. The distinction between investment and speculation in common stocks has always been a useful one and its disappearance is a cause for concern. In most periods the investor must recognize the existence of a speculative factor in his common stock holdings. It is his task to keep this component within minor limits, and to be prepared financially and psychologically for adverse results that may be of short or long duration.

There is intelligent speculation as there is intelligent investing. But there are many ways in which speculation may be unintelligent. Of these the foremost are: (1) speculating when you think you are investing; (2) speculating seriously instead of as a pastime, when you lack proper knowledge and skill for it; and (3) risking more money in speculation than you can afford to lose."

-Benjamin Graham, The Intelligent Investor

Source: Hargreaveslansdown.

We still know the same things, I believe.

• Interest rates are still close to zero in many parts of the world, despite strongly recovering ‘growth’ and real concerns about rapidly rising inflation

• Central banks, while still pouring out the cash through monetary spigots have absolutely no room for manoeuvre, should anything bad happen, weaker growth, stock market sell-off etc

• Far too many ‘growth’ stocks have huge growth multiples, (not delivered yet) baked in current stock prices, resulting in a terrible skew of disappointment potential over actually achieving better than projected amazing growth, with book values for US stocks at a whopping 2.5x. Very slim pickings for Benjamin Graham’s margin of safety rule, looking for sub 1X book opportunities in todays’ world.

• While the US equity market has appreciated consistently more than the rest of the world markets such as the UK, which is seemingly considered ‘cheap’ and ‘good value’ by all good pundits, the fact that every 10% down correction in US stocks for decades has seen 10%+ down corrections as well, seems far less appreciated or prepared for

• Commodities, RELATIVE, to equity and bond markets, especially precious metals are historically cheap

• Geo-politics, arguably always in play, seem far more contentious than in recent decades, with supply and trade issues in full view

The HindeSight portfolio’s addition this month of SSE, simply adds another, typically referred to as, defensive stock, it supplies essential goods, classed as Utilities, to go with the current holdings of food, mining, pharma, tobacco and telecom. The dividend yields range from 3.5-12%, with an average of 6.40%, certainly better than junk bonds and still better than inflation, but I believe all have growth potential as well. At least I would hope that Benjamin Graham would not be turning in his grave and understand the methodology of the HindeSight model at the current time.

I think the second paragraph in Graham’s quote could easily sum up the current crypto-currency market. There are probably no better trading markets than the cryptospace, with daily and weekly volatility that other markets can only reminisce about. It has almost 24/7 trading hours, reasonable liquidity at price, without too much gap volatility, (Can you get out at your stop price, if needed?) but it is not a long-term investment opportunity by my metrics.

There are many ways in which speculation may be unintelligent;

• Speculating when you think you are investing

• Speculating seriously instead of a pastime, when you lack proper knowledge and skill for it

• Risking more money in speculation than you can afford to lose

I believe that probably sums up 80% of people, active in the Crypto trading space currently, but to the ex-colleagues with 20+ years trading experience in interest rates, commodities or FX that are making good money, hat tip to you, but I know none of you consider it investment, by any stretch.

Of course, there is some margin of safety, even if it’s just a money-launderer’s 20% discount rate and thrown in some electricity costs, but that level is far below current market prices so the speculation premium is very high. Whenever I ask myself, “What is more likely to happen, world governments all create their own digital country currencies (still printable of cost-how else to you pay your debts), with full state backing or do they relinquish that right to the masses always answers my long-term thoughts on Crypto.

HINDESIGHT PORTFOLIO SELECTION

23/09/2021, BUY-OPEN, 1665P

SSE Plc, is one of the top six energy companies in the UK, headquartered in Perth, and can trace its origins back to the 1940s before amalgamations.

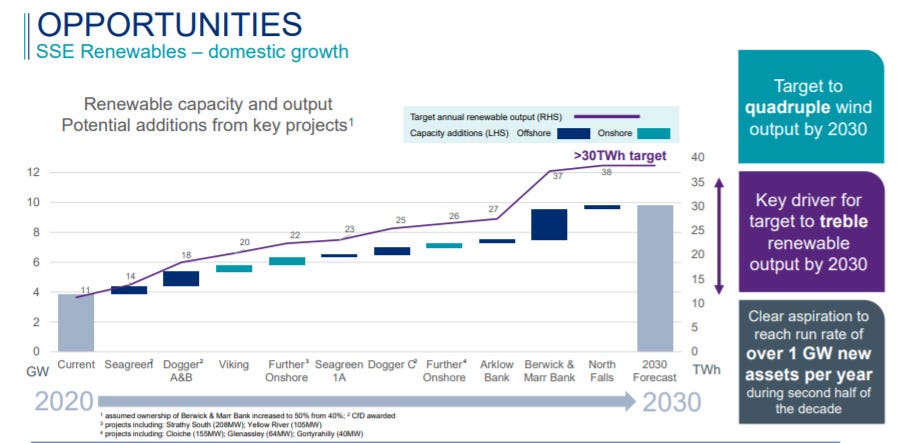

What do we need to know about SSE as we add it to our portfolio. It’s yet another defensive stock, you don’t get much more defensive that utilities. But, it pays a 5% dividend, as a long-term company, and is heavily investing in renewable energy to provide the power and electricity of the future, so I believe it actually has real growth potential. Renewables are clearly the future and we are going to better at it, whether it’s wind, solar or hydro, and if the holy grail of being able to harness and store, the world will be in good order by the second half of the 21st century.

It looks like there is every possibility that competition within the energy space will contract again as smaller companies go into default, with the recent input price rise, mainly of imported natural gas. As mentioned previously, the 70+ companies that were in existence at the start of 2021, may well be under ten by year end. I would hope that SSE have done a better job of hedging their forward exposure than the new junior players, which may see SSE pick up many new customers as Ofgem is forced to take over and distribute customers whose supplier has gone bust. Obviously, it’s not good for the consumer for the oligopolies to re-emerge but as is often in crises, the big firms survive, the small ones don’t. In 2004, the big six, provided 100% of UK power, last year it was less than 70%. But, bad for consumer, good for the providers maybe?

In recent SSE news, we clearly have activist investor Paul Singer’s Investment Management with a large stake, calling for a break-up, with the belief, the parts value are greater than the sum of today’s market capitalisation. As well as new deals being done for renewables in Japan, as its nuclear industry has never really recovered from the Fukushima disaster in March 2011, makes SSE a worthy addition to the portfolio this month.

Visit hindesightletters.com for more information