HindeSight Investment #98 March 2023 - Newsletter - Read Here

To read next month’s HindeSight letter on the day it’s released please subscribe for the price of a cup of coffee per month, only £4.99 or save by subscribing yearly. More information at the bottom.

CONTENTS

OVERVIEW

INVESTMENT INSIGHTS

PORTFOLIO UPDATE

HINDESIGHT DIVIDEND UK - PORTFOLIO #1 MAR 2023

OVERVIEW

Since the beginning of time banking has made and lost fortunes for those involved in its activities. This has happened on a fairly regular basis for hundreds of years. One of the best examples was of the great Florentine banking dynasties of the middle ages. Established to assist in the new world of industry and growing cross border trading the great names of Medici, Bardi and Peruzzi to name a few, sprung up accepting deposits from wealthy nobleman and merchants which they lent to monarchs and the papacy to finance international and religious conflict. Many of these were created as family businesses with unlimited liabilities and had numerous branches across Europe. Although the loans were often made to the AAA credit monarchs of the day, the doors of the Bardi and Peruzzi banks closed between 1343 and 1346. This was mainly due to the non-repayment of gigantic loans by King Edward III of England which he had taken to finance The Hundred Years War with France. The Spinelli bank collapsed in 1456 as Pope Calixtus III reneged on his debts. Even the Medici bank, the largest and wealthiest in the 15th century credited with the financial innovation of the bill of exchange did not survive and folded in 1494. Many products created in the Middle Ages were to facilitate trade without carrying large quantities of gold specie and to avoid the receiving of interest usury still forbidden by most religions. The two belligerents of the English War of the Roses, The Lancastrians and the Yorkists who finally settled their differences at Bosworth Field nine years earlier were unable to repay their loans to the Medici bank which was the final nail in the coffin for the Citibank of the time.

As the medieval goldsmiths realised, (republished this week from HindeSight Archive-sign up free on Substack) the basis of Fractural Reserve banking is simplicity itself. You receive deposits for which you pay X %, with which you make loans at X+ %. The difference in the maturity of the deposits and loans, the spread and the number of loans you make levered off the deposit base all factor into the equation of profitability. As does the correct analysis of risk and the diversification in determining the margin for potential defaults. Every bank failure in history has resulted from the incorrect analysis of the potential changes in these factors.

While some seemingly conservative banks will fail at times as well as the more foolhardy; poor forecasting abilities are always at the fore front. In the pursuit of profits amid heavy competition, bankers find new ways and hopes to avoid natural business cycle events. Not all as stupid as others. (HindeSight Letter 2009)

Banking has been an inherent factor for economic growth for centuries, but unfortunately the human race is condemned to making the same mistakes as the past. The crazy month of March has seen two high profile cases of bank failure, Silicon Valley Bank and Credit Suisse.

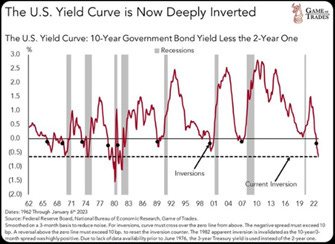

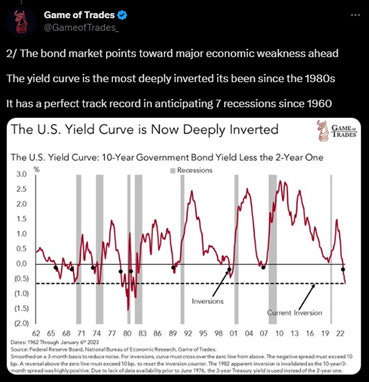

Periods of time when central banks raise short-term interest rates causing yield curve inversion, (where short rates are higher than longer rates) usually leads to something breaking in the banking industry, whether by slowing economic growth as the risk-free interest rate increases lead to company bankruptcies or simple maths deposit/liability and poor decisions.

Banks’ modus operandi is to borrow short (dated such as deposits) and lend long (dated-such as loans, mortgages etc). With a normal yield curve, where long rates are greater than short rates, the spread is called the Net Interest Margin, (NIM) and assuming that correct credit analysis is done, that is the route to profitability for banks. During a curve inversion period such as now, due to the central banks having to raise rates aggressively to ‘combat’ the inflation, (that they created in the first place, by the last decade and a half of their insane money printing experiment), that NIM is now negative, in theory. Obviously, they have been loath to raise deposit rates quickly to their customers for this very reason, but competition for deposits either from other banks or, especially in the US, money market funds forces their hand. Moving from bank risk to government risk is key to the savvy investor, mind-blinding really to see tech CEOs queuing to get their cash deposits out of Silicon Valley branches. When I sold my last house, the cash was in my bank for less than a day before I bought UK Govt T-bills. Of course, that is not always possible for smaller deposits or with some banks.

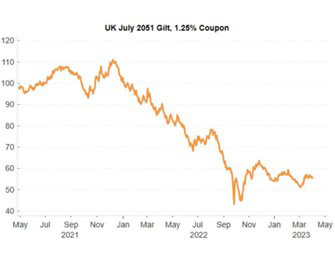

We must always remember that bank’s assets are their loans and their liabilities are customer deposits. If the loans are looking at risk or deposits are hard to maintain, or you have to pay up to keep them, then you are in trouble. In the case of Silicon Valley Bank, having too much concentration to tech start-ups for your loan book, and deciding it’s a great plan to invest your deposits in too many long-dated government/quasi government bonds at the top of a 40 year bull market, (rather than short-dated paper) with substantial price risk, when you have to liquidate them led to their demise. Not exactly rocket science, just poor management decision making. This price decline in long dated bonds, when you needed liquidity didn’t help the UK pension industry last autumn either! Maybe their ‘Monroe bond calculator’ was on the blink, or couldn’t compute the actual potential price losses, when and not if interest rates normalised.

30-year UK Gilts, price chart.

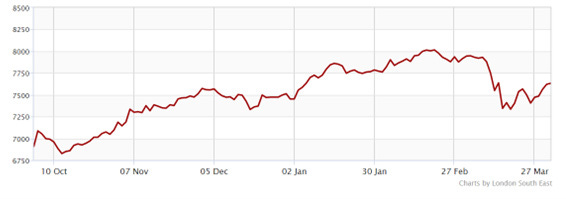

Arguably, the SVB failure/bank run was also a crisis of confidence as too many depositors rushed to withdraw funds, forcing sales of long-dated assets realising huge losses, rather than concern about loan portfolio. The buyer of some of SVB loan book seems to think so….(at whatever discount they got). As for the deal of the century by HSBC to get SVB UK’s arm for £1, the less said about the better. That must have taken real wheeling and dealing by the UK authorities….I don’t think.

First Citizens Banc Shares, price, 6-month

It will happen again. Ineffective and “closing the barn door after horse has bolted” regulators and human naivety-lack of experience/greed ensure this.

Nice to see my old trading stomping ground of US interest rates make history. I remember those volatile days in the mid-80s as a young US government bond trader. Quite a change for the traders/investment managers of today realising that interest rates can move that quickly after all.

On the geopolitical front, seemingly out of the mainstream western media is the news that China has brokered a deal between Saudi Arabia and Iran, restoring diplomatic relations after a seven year hiatus and decades’ long rivalry, marred by distrust and sporadic bombardments. The possibility that there could be an amnesty between the heart of the Sunni and Shia Muslim sects remains to be seen, but the fact that China could be the new “world peace” broker is ominous to our longstanding belief regarding US and western hegemony. With Iran and Saudi now moving to membership of the Shanghai Co-operation.

Zelensky, potentially seeing the cards on the table, seems open now to talking with China, who are discussing a peace plan for the Russia/Ukraine conflict. He is obviously worried about the waning support from the west especially with Republican opposition to more war weapon billions. No doubt, the ‘compromise’ deal with China’s brokering will be the similar to what was on the table from Russia last March before Boris Johnson and the US persuaded Ukraine to fight a futile war, with a year of death and destruction as a result.

Maybe China has figured out that continuing a futile war and nuclear escalation isn’t part of their grand plans for world domination and they are having to get involved because the US doesn’t seem to have the same clue/ thought. Another fine mess, you have got us into…

As high stakes US geopolitical poker games go, this is clearly not panning out as planned with China, Russia, Iran, Saudi and Africa forming alliances in the new order. With Iran and Saudi now moving to membership of the Shanghai Co-operation Organisation, that would be most of the world’s fossil fuels and mineral deposits the other side of the new Curtain and a very much declining US hedgemoney/Nato west on the other. The Economist’s comment “that conflicting visions among the growing membership mean it poses little threat to the West” sounds a bit Bob Hope to me!

I can’t help thinking that the iceberg is coming into full view and we are ploughing on regardless…

INVESTMENT INSIGHTS

The old adage as every trader knows, “up by the stairs, down by the elevator” is in full view in most stock markets this March with a plethora of bad news, mainly from the headlines of bank failures took us back to January 1st levels. It doesn’t seem only last month I wrote; (small trumpet blow)

“The liquidity seen in January that floated all boats, gold, bonds and equities has probably run its course for the time being. After all, bonds and stocks most often have some inverse correlation. The enthusiasm for ‘cheap’ stocks worries me and the almost 7% return in FTSE100 year to date as bonds falter brings lightening up/trimming/rebalancing thoughts to mind”.

-HSL Feb 2023

For me, one of the major concerns with any rallies in the world’s equity markets is that they still remain historically expensive on most standard metrics, such as revenue/ price. The reversion to the mean over time will be understood in time that the cost of risk-free capital has changed substantially over the last year and this blows apart the comparisons of value over the last decade. Too many scribblers always compare the relative ‘cheapness’ of UK equity markets to their US counterparts, but the high correlation factor on any down move never feels great.

The Permanent Portfolio admirably demonstrated it’s all weather investment philosophy this month.

Despite most stock indices being down 4-5%, bonds were up 3.5% and gold was up 5%, to make a positive return this month. All of our work at Hinde Capital over the years, (which hopefully readers are enjoying with our Friday archive posts), some of the most notable has been to demonstrate that, while the Permanent Portfolio will never be the biggest winner in great investment years, its ability to smooth the return profile and mitigate the big losses is paramount to long-term compounding. Alongside the HindeSight Equity model portfolio, of course.

Many investment managers, especially interest rate traders have had their work cut out for them in that last six months, volatility back with extreme vengeance, but that’s what happens when the yield curves go through an inversion period, as central banks drive short-term rates up to ‘combat’ inflation. No sooner do you think you are on the trend, it reverses and runs you over and the margin call police are at your desk. The graphs below suggest clearly-deep inversions are seen before recessions most of the time. The process of lower stock prices and recessions force the central banks to go from rate rises to rate cuts and the inverted curve normalises. During this period of time, gold as an asset class outperforms equity markets. As we found over 15 years of travelling the globe for Hinde Capital, gold is typically very under represented in portfolio allocations, but the facts are very clear with the current macro scenario.

PORTFOLIO UPDATE

There were two additions to the portfolio this month;

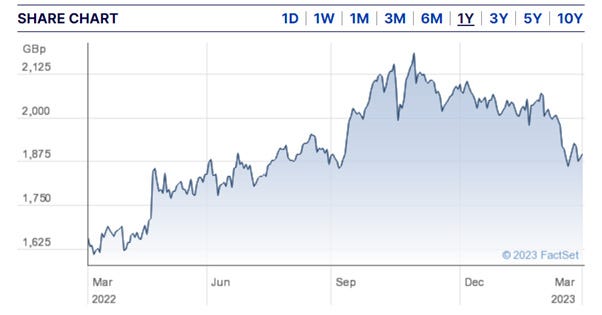

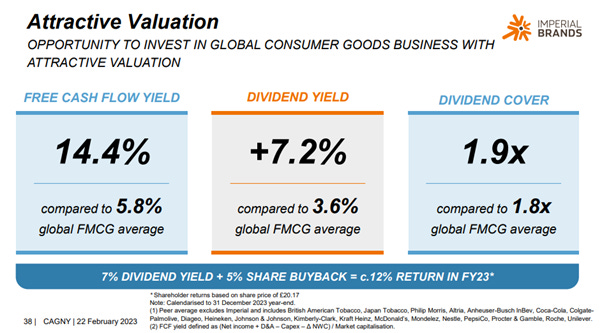

• Imperial Brands Plc 16/3/2023, 1875p Dividend Yield 7.45%, P/E 7.15

• Legal & General Plc 21/03/2023, 234p Dividend Yield 8.32%, P/E 5.98

The 7% rout in the general UK indices this month, roundtripping the year to date change back to unchanged has given opportunities to add to the portfolio. But, we are glad to be adding two high dividend payers, with low price/earnings ratios and solid balance sheets and cash flow. These well-known FTSE100 big caps are clearly defensive model allocations. With the change in the risk free interest rate above 4% now, there will ultimately be challenges for many companies that have high P/E ratios and low dividend yields, with earnings growth the biggest challenge going forward. The margin of safety in both IMB and LGEN relative to recent history is considerable and we would expect the 9-12 month return, including dividends to be superior to the general index.

Imperial Brands stock price, 1-year

Legal & General stock price, 1-year

HINDESIGHT DIVIDEND UK PORTFOLIO # 1 (MARCH 2023)

Visit hindesightletters.com for more information

To read next month’s HindeSight letter on the day it’s released please subscribe for the price of a cup of coffee per month, only £4.99 or save 2 months with a yearly subscription.

WHY SUBSCRIBE TO THE HINDESIGHT LETTER?

INVESTMENT INSIGHTS

Not only do we break down the reasoning behind our monthly share choices, we explain the methodology behind investing so you will learn more about strategies and how they impact your portfolio. Investing is like anything else, the more you know, the better you'll be at it and the better your decision to invest will be.

EMAIL ALERTS

You will also receive timely email alerts detailing portfolio changes to the HindeSight Dividend Portfolio #1, that covers FTSE350 stock as suggested by our Hinde Dividend Matrix and seasoned money managers. These are for immediate changes in opening or closing a position.

HINDESIGHT PORTFOLIO SELECTION

In our monthly HindeSight portfolio selection article we cover in-depth and in plain English, our reasons why we added the previous share to our portfolio with additional insights and performance data that's usually reserved for the trading floor.

OVERVIEW

Our overview features analysis, research & opinion on the latest news and current affairs and is a window into understanding factors that shape markets.

WHY CHOOSE US?

HindeSight Letters is a unique blend of financial market professionals – investment managers, analysts and a financial editorial team of notable pedigree giving you insights that never usually make it off the trading floor.

We help our paid subscribers have 100% control to build their own portfolios with knowledge that lasts a lifetime and all for the price of a good coffee a month - just £4.99. Our history is there for all to see, measure and research.