Death of banking?

For savers anyway...

It's a question that plagues many people who are looking to save their money: should you invest it or stick it in a bank account? The answer is complicated and depends on a variety of factors, including your risk tolerance, investment goals, and timeline. But one thing is clear: over the long-term, investing has historically provided a better return on investment than sticking your money in a savings account. At today’s rates even with the likes of Apple starting a ‘bank’ with their headline grabbing 4.5% deposit rate, you might have to put some money somewhere just for your life to function, but Apple’s not a bank, so will the millions of people that jump ship need a traditional bank anymore?

Let's start by looking at the historical interest rates for savings accounts. According to data from the Federal Reserve Bank of St. Louis, the average interest rate on savings accounts in the United States was around 0.16% in 2020. This is a far cry from the interest rates of the 1980s, when savings accounts were yielding over 10% interest. In fact, interest rates have been steadily declining since the 1980s, making it difficult to earn a decent return on investment through savings accounts alone.

Investing, on the other hand, has historically provided a better return on investment than savings accounts. The stock market, for example, has returned an average of around 10% per year over the long-term, despite occasional downturns and volatility. This means that if you had invested $1,000 in the stock market in 1980, it would be worth over $20,000 today. Of course, there are no guarantees when it comes to investing, and the stock market can be volatile in the short-term. But over the long-term, investing has proven to be a reliable way to grow your money.

There are a number of benefits to investing over saving, especially when interest rates are low. For one, investing allows you to take advantage of compound interest, which means that your returns can grow exponentially over time. Using an ISA can help you avoid the tax you’d encounter on your savings (if they are in a non-ISA account). Investing also allows you to diversify your portfolio, which can help reduce risk. By investing in a variety of stocks, bonds, and other assets, you can spread your risk around and avoid having all your eggs in one basket. This can help protect your investments from the ups and downs of the stock market.

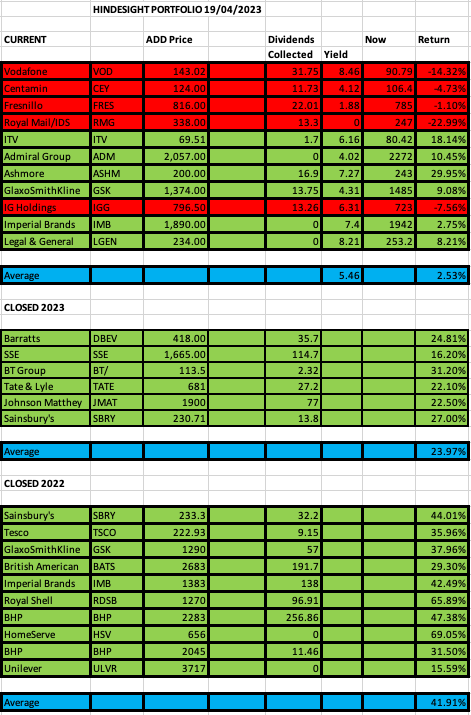

Banks provide OK rates of interest, but as you can see above from the weekly ‘best buy’ table, they’re more than happy to make sure it’s only for a certain amount per month, for a certain amount of time, or any other option that makes them come out on top. Sure they’re offering an on demand service but it feel a lot like they’re losing the plot on what customers want and why they want it.

Most people will need some kind of money holding account to manage their life - have their salary paid into, pay their bills, give them somewhere to put money. But aside from that, what’s the point? Some basic accounts (oversimplified): you need £2000 per month to live and after tax get a £3000 monthly pay packet. Why drop the spare £1000 into a bank when you could have (see our table) set up for an ISA and give you much more, with the only penalty that you’ll lose some allowance if you take it out.

If you have a lot of money, then banks are chomping at the bit to get some of it and will court you to get you on board. If you have *some money (£100 - £2000 per month spare) then you’ll have to weigh up the options of chucking it into a bank (sure it’s the easy/lazy option) or working your money a bit to try to provide a better return, and more money. We’re very much on the side of the people who have *some money to invest, though there’s quite a few people who have *a lot of money that also follow our letter. Look again at the table above. Anyone have a bank that can match that?